Coherent's Vertical Integration Strategy

Coherent makes more of the optical stack in-house than any competitor. We walk through the business, the growth vectors, and whether breadth beats depth.

Quick hits:

Coherent makes its own EMLs, VCSELs, silicon photonics, and finished transceivers. It’s hard to find another public company that touches this many layers of the optical stack.

Six-inch InP is ramping across four fabs with yields management says exceed 3-inch. The performance comparison against Lumentum is still playing out.

Five growth vectors stacking: transceivers, OCS, DCI, CPO, thermal. Management says CY2026 is mostly booked and CY2027 is filling fast.

Breadth vs. depth is the real question. Does a hyperscaler want one partner for everything, or best-in-class at every layer?

We’ve covered Lumentum’s and Broadcom’s AI optical infra businesses so far. Lumentum is a shooting star thanks to its laser performance plus tailwinds of industrywide supply scarcity. Broadcom dominates the datacenter networking silicon (Tomahawk switches, 1.6T DSPs) and is pushing direct-attach copper in scale-up for as long as physics allows, even as it builds CPO technology (lasers included) for optical scale-up.

Time for Coherent.

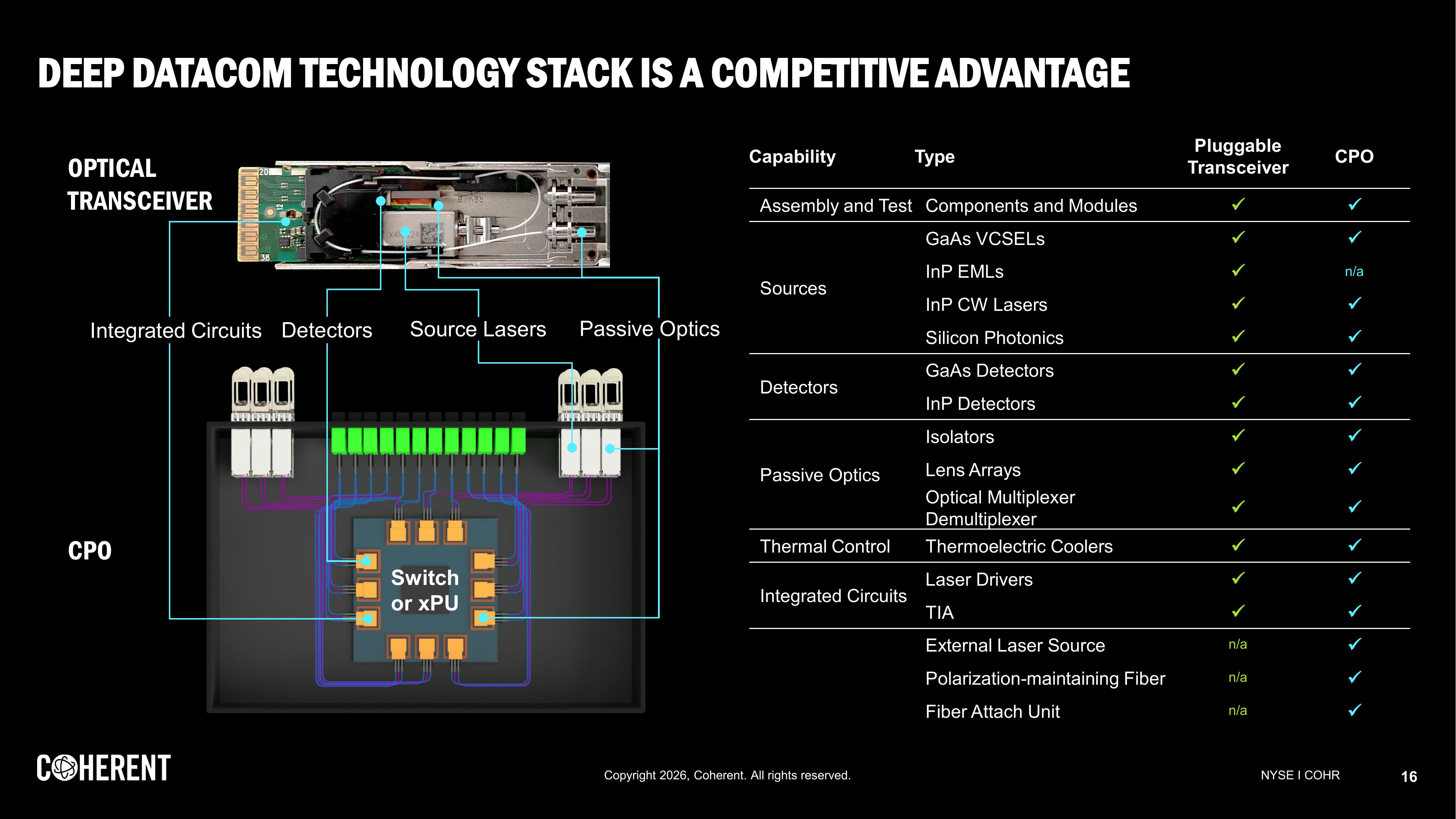

Coherent’s angle is vertical integration across the photonics value chain. The company designs and manufactures InP-based EMLs and CW lasers, VCSELs, silicon photonics, detectors, and finished transceiver modules in-house.

That puts it in competition with Lumentum, Broadcom, and Sumitomo at the component layer, and with module vendors like InnoLight and Eoptolink at the transceiver level. The stock has run from $45 to $250 in fifteen months and still trades at a lower forward multiple than Lumentum.

In August 2025, Coherent began production on what management calls the world’s first 6-inch indium phosphide production platform in Sherman, Texas and Jarfalla, Sweden:

If yields hold, that should materially improve Coherent’s cost structure and add meaningful InP supply to an industry that is currently constrained. How that affects pricing dynamics across the laser supply chain is one of the key tensions we’ll explore below.

Coherent’s vertical integration means it can supply components, modules, or systems across virtually every optical architecture a hyperscaler might adopt, from pluggable transceivers today to co-packaged optics and optical circuit switches tomorrow:

The bull case is that this flexibility becomes increasingly valuable as datacenter optical needs diversify. The bear case is that hyperscalers prefer to unbundle and multi-source each layer, buying best-in-class lasers from Lumentum, DSPs from Broadcom, and modules from whoever is cheapest.

Let’s walk through the business, the growth vectors, and the tensions that matter.

NFA, DYDD.

Coherent Corp

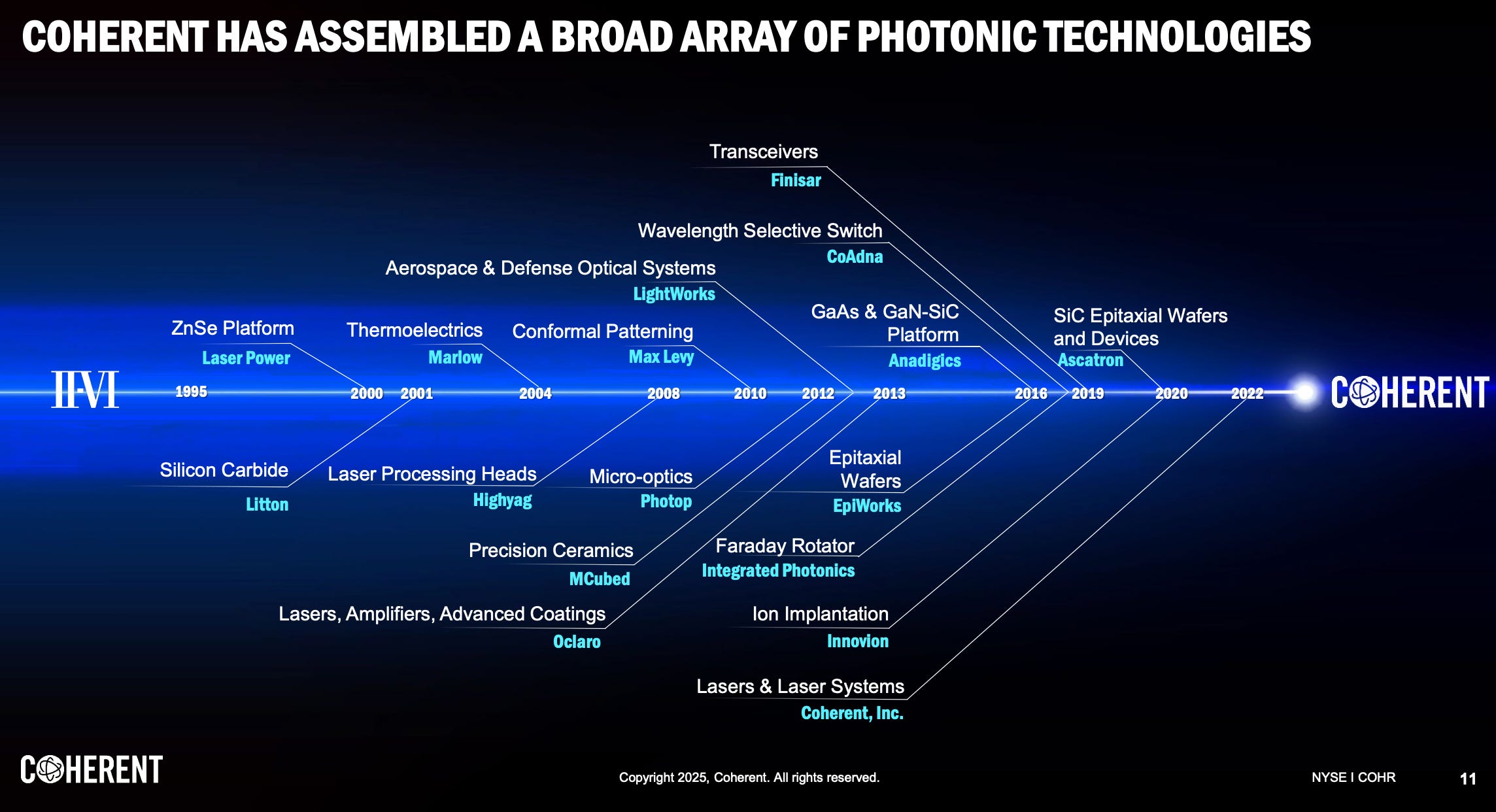

Coherent’s backstory begins with II-VI Incorporated, founded in 1971 and named after the II-VI compound semiconductor groups on the periodic table. Naming is hard.

II-VI’s original business focused on supplying engineered semiconductor materials and optical substrates that form the foundation of lasers and other photonic devices. Thus, the company operated at the lowest layer of the value chain, upstream of components and with limited exposure to finished products.

There have been many acquisitions along the way:

A few notable ones.

Finisar was acquired in 2019 for ~$3.2B. It was a leading manufacturer of optical transceiver modules at the time and brought significant VCSEL capacity for 3D sensing (for Face ID). The deal extended II-VI from raw materials into finished modules and added scale in hyperscale networking.

Coherent Inc. was acquired in July 2022 for ~$6.6B. Coherent was a storied laser systems company, founded in 1966, that built the first commercial CO2 laser and grew into a global leader in industrial laser systems, especially after acquiring Rofin-Sinar in 2016. It brought complete laser systems for cutting, welding, semiconductor lithography annealing, and display manufacturing, moving II-VI from components into full systems.

So II-VI started as a materials maker and eventually expanded to add photonic products and laser systems capability. They rebranded the parent company II-VI as Coherent Corp. in September 2022.

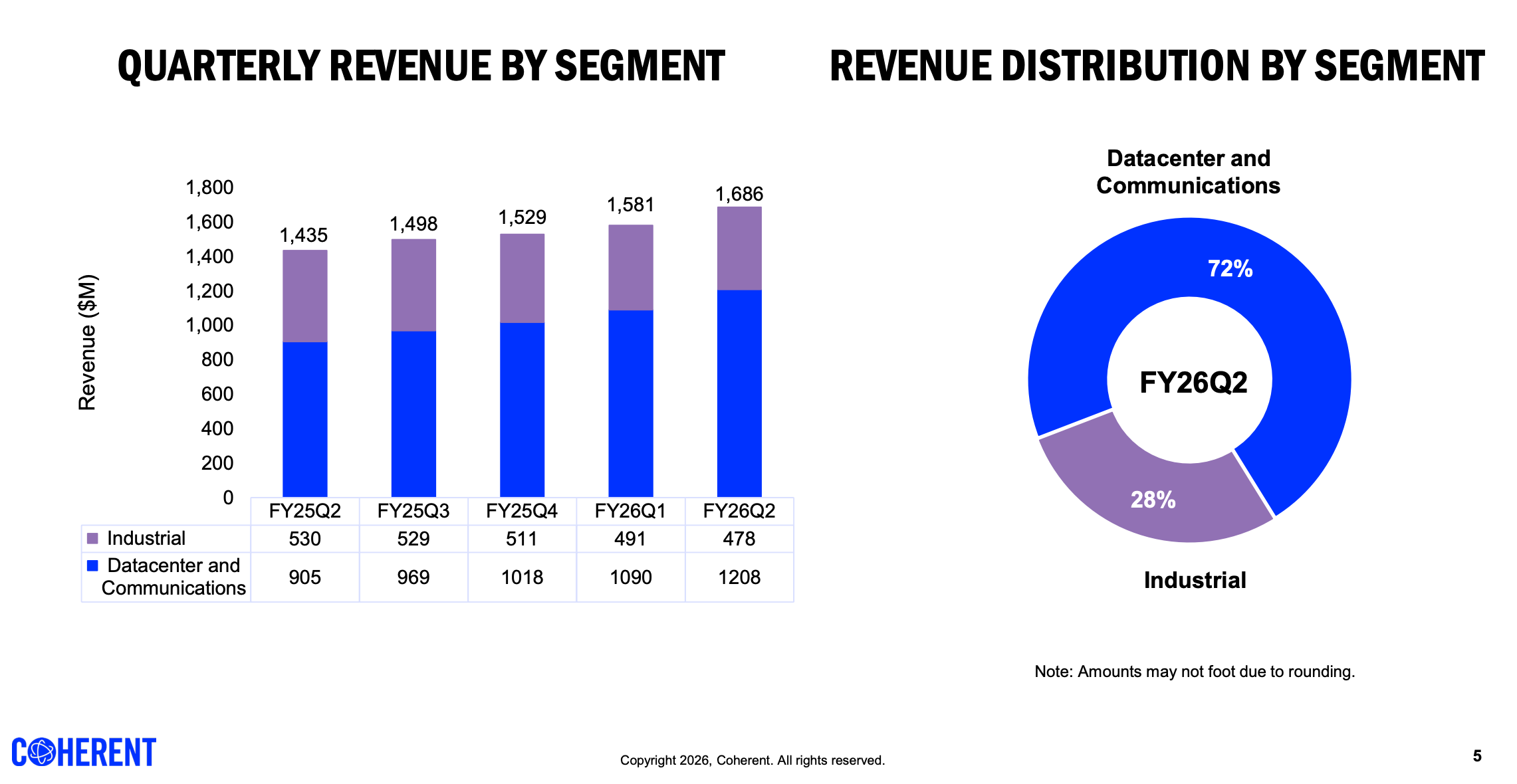

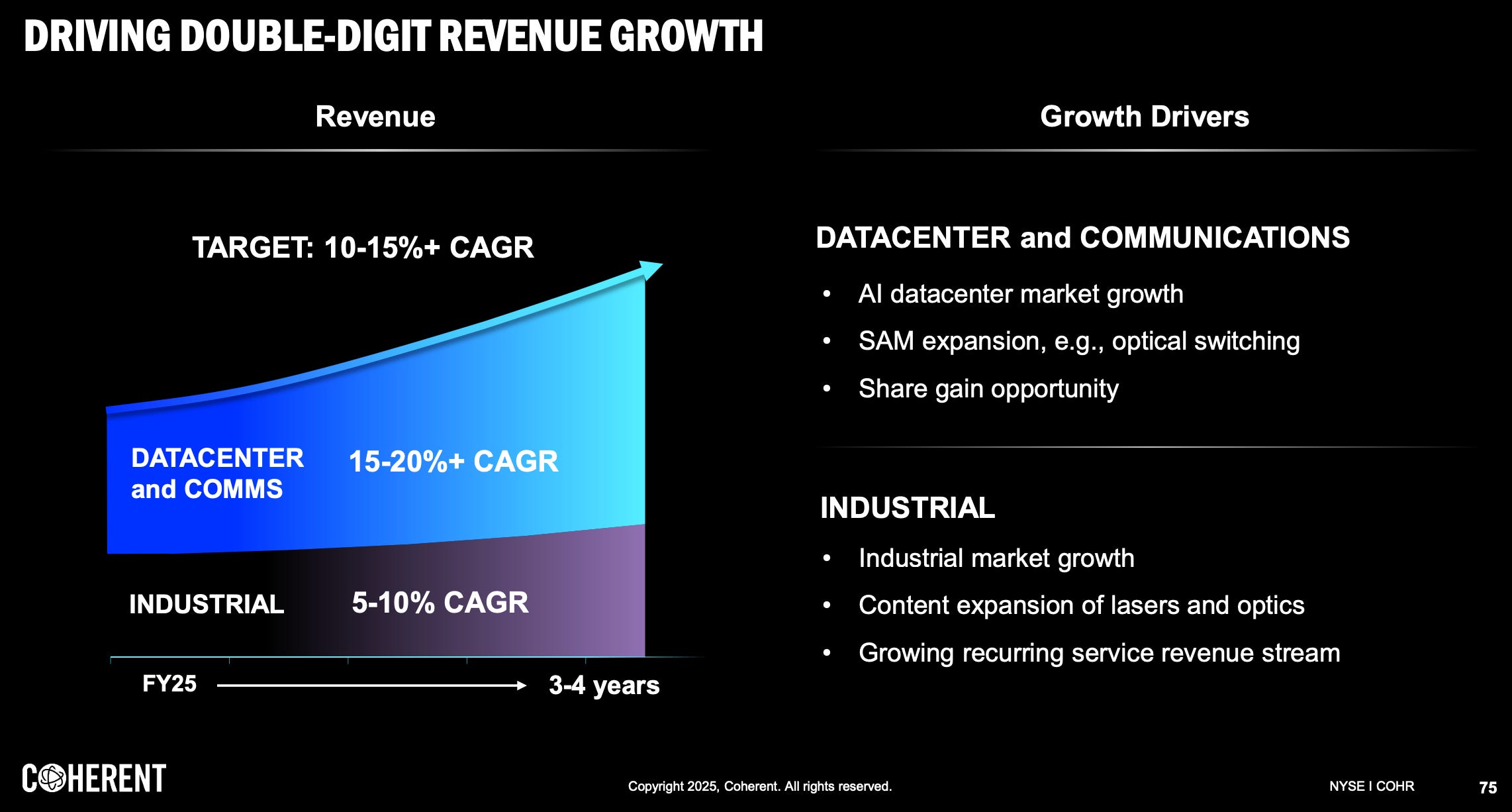

The result is a company with two distinct lines of business. ~72% of revenue comes from Datacenter & Communications (DC&C), the high-growth segment riding the AI optical buildout. The remaining 28% is Industrial; lasers for semiconductor equipment makers like ASML and Applied Materials, excimer lasers for OLED display fabs, silicon carbide substrates, and specialty materials.

The industrial business is slow growth, but it’s profitable, sticky, and generates nice margins. The slide above suggests Industrial is shrinking QoQ, but the 2025 Analyst day suggests Coherent thinks it can still grow 5-10% CAGR over the next 3-4 years.

Drag on the AI story? Or a diversified base? I tend to be comfortable with the latter — good source of margin dollars.

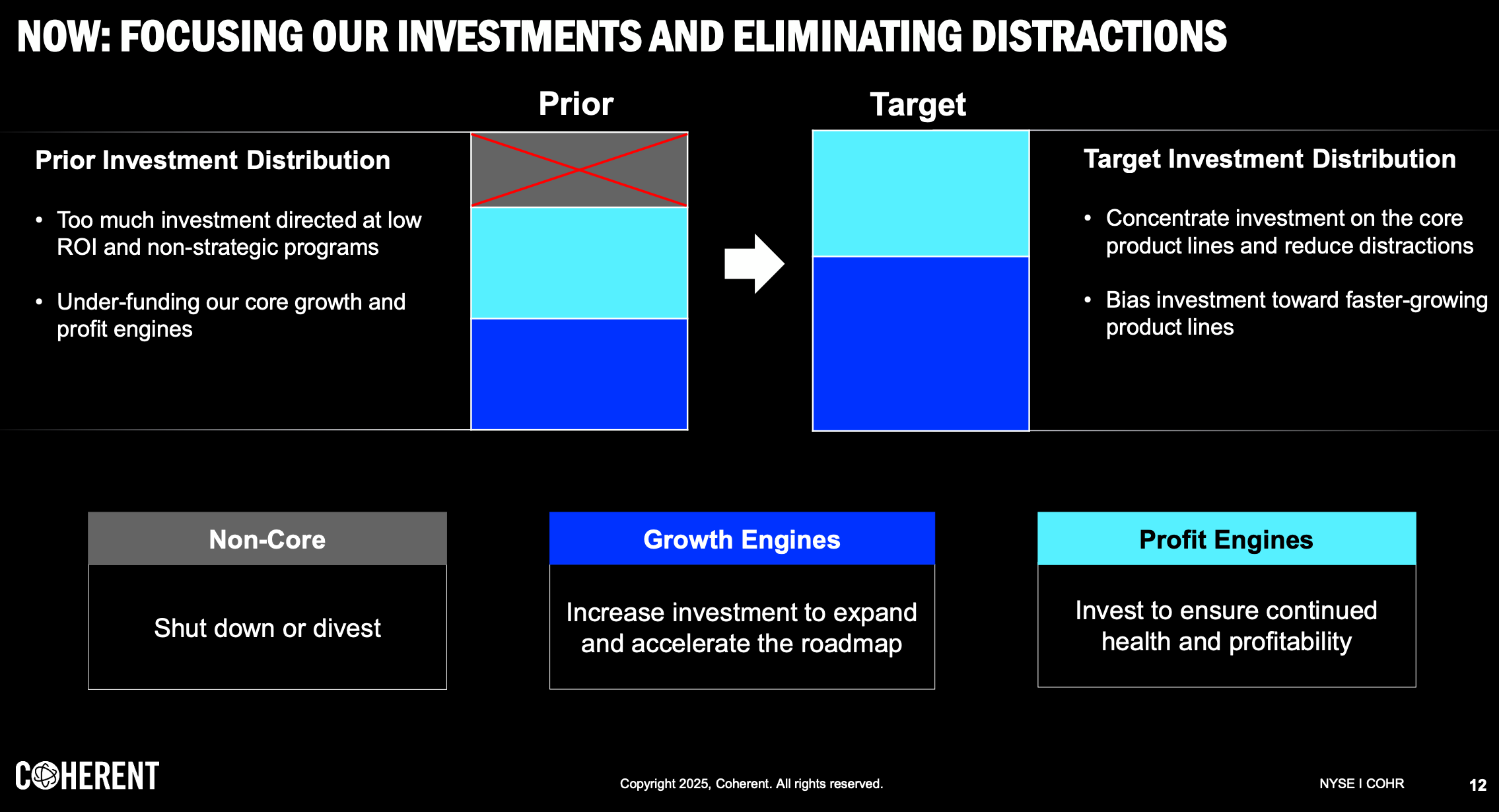

Coherent CEO Jim Anderson’s mandate is to reshape Coherent from a leveraged, margin-constrained conglomerate into a focused AI photonics platform, and the company is making solid progress. Revenue has grown from $4.73B in FY2024 to a ~$6.7B annualized run rate, while gross margins have expanded by roughly 500 bps to ~39% and EPS has scaled from $1.21 to over $5 on a run-rate basis.

At the same time, leverage has been reduced from over 3x to 1.7x, alongside a series of divestitures and footprint reductions to simplify the business:

Coherent bonus points: Was recently included in the S&P 500 and a $2B equity investment plus multibillion dollar supply agreement with Nvidia.

Vertical Integration

Coherent claims to have the broadest photonics portfolio in the industry.

Let’s walk through it.

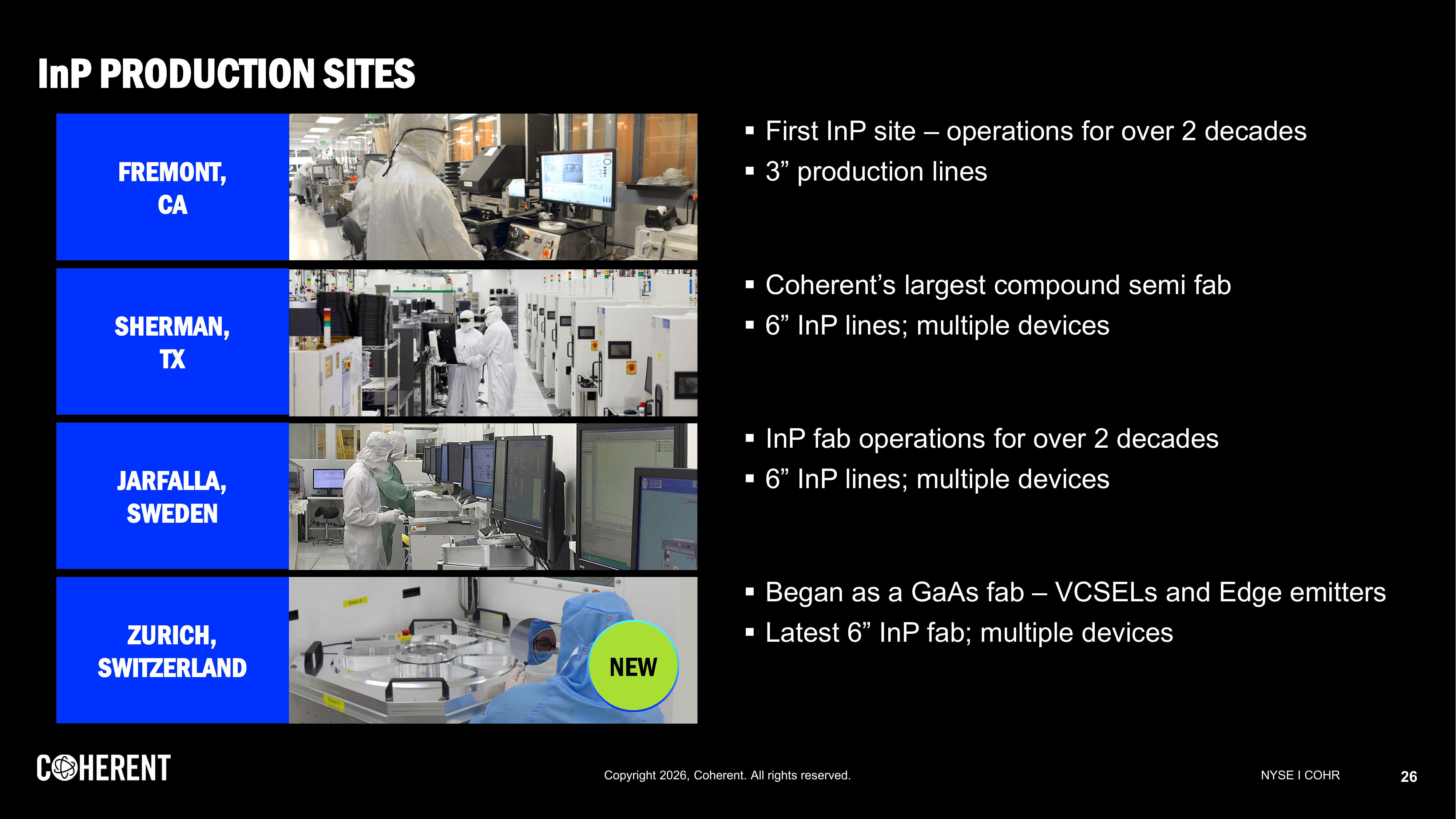

First, indium phosphide (InP). Coherent has over 20 years of in-house InP capability spanning epitaxial growth, laser fabrication, modulators, photodiodes, and integrated subsystems.

One important clarification: Coherent does not grow its own raw InP crystals. It purchases InP substrate wafers from external vendors under 3-to-5-year supply agreements, then performs epitaxy and device fabrication in-house. This is the same fundamental supply chain dependency that Lumentum and Broadcom face, though Coherent has locked in multi-year contracts with multiple 6-inch substrate vendors to mitigate it. Worth noting that Coherent does grow its own SiC and GaAs crystals internally; it is specifically InP substrates that are sourced externally:

Gianmarco Conti, Analyst: Gianmarco from Deutsche Bank. You’re expanding indium phosphide capacity, but the raw indium feedstock is roughly 70% sourced from Chinese zinc smelters, which are now subject to export permit requirements with multi-month processing times. I guess my question is, how much visibility do you have on indium supply for the next 12 to 24 months? And are you actively diversifying sourcing away from China? Or do you hold strategic inventory buffer?

James Anderson, CEO: We actually have a very diversified supply chain for indium phosphide substrates. We have -- and I think I’ve shared this in the past, we have over five different substrate suppliers today, and we work with those suppliers, not just on the next -- you mentioned next 12 or 24 months. We don’t work on just next 12 to 24 months. We work on the next like three to five years of capacity that we’re going to need. So we have, in some cases, very long-term agreements in place. And that includes not just the substrates, but all the key inputs that go into that. So we believe that we have very good visibility into substrate supply. And so that capacity expansion that Beck showed is we have commitments from our suppliers to supply the necessary indium phosphide substrates to support that.

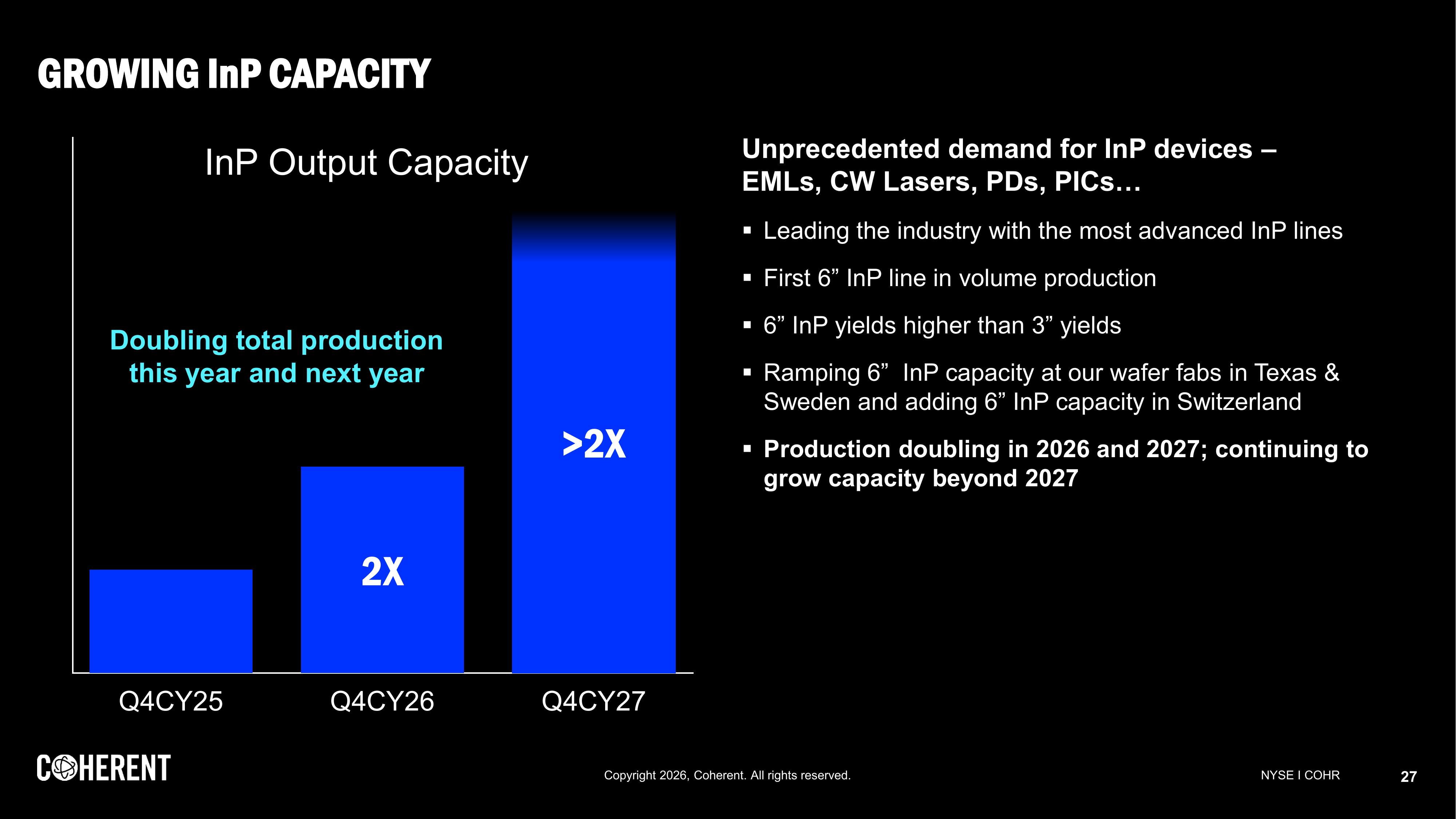

The 6-inch InP production platform is an important topic. Management calls it the world’s first, and it is now ramping across four sites: Fremont, California (3-inch legacy); Sherman, Texas; Järfälla, Sweden; and Zürich, Switzerland (newest addition). The economics, per management, are roughly 4x the devices per wafer at about half the cost compared to legacy 3-inch lines, with capacity doubling this year. If yields hold at scale, this could result in competitive cost structure relative to Lumentum (which is migrating from 3-inch to 4-inch) and Broadcom (believed to be on 3-to-4-inch). The timing of those yields is one of the main questions we’ll look at below.

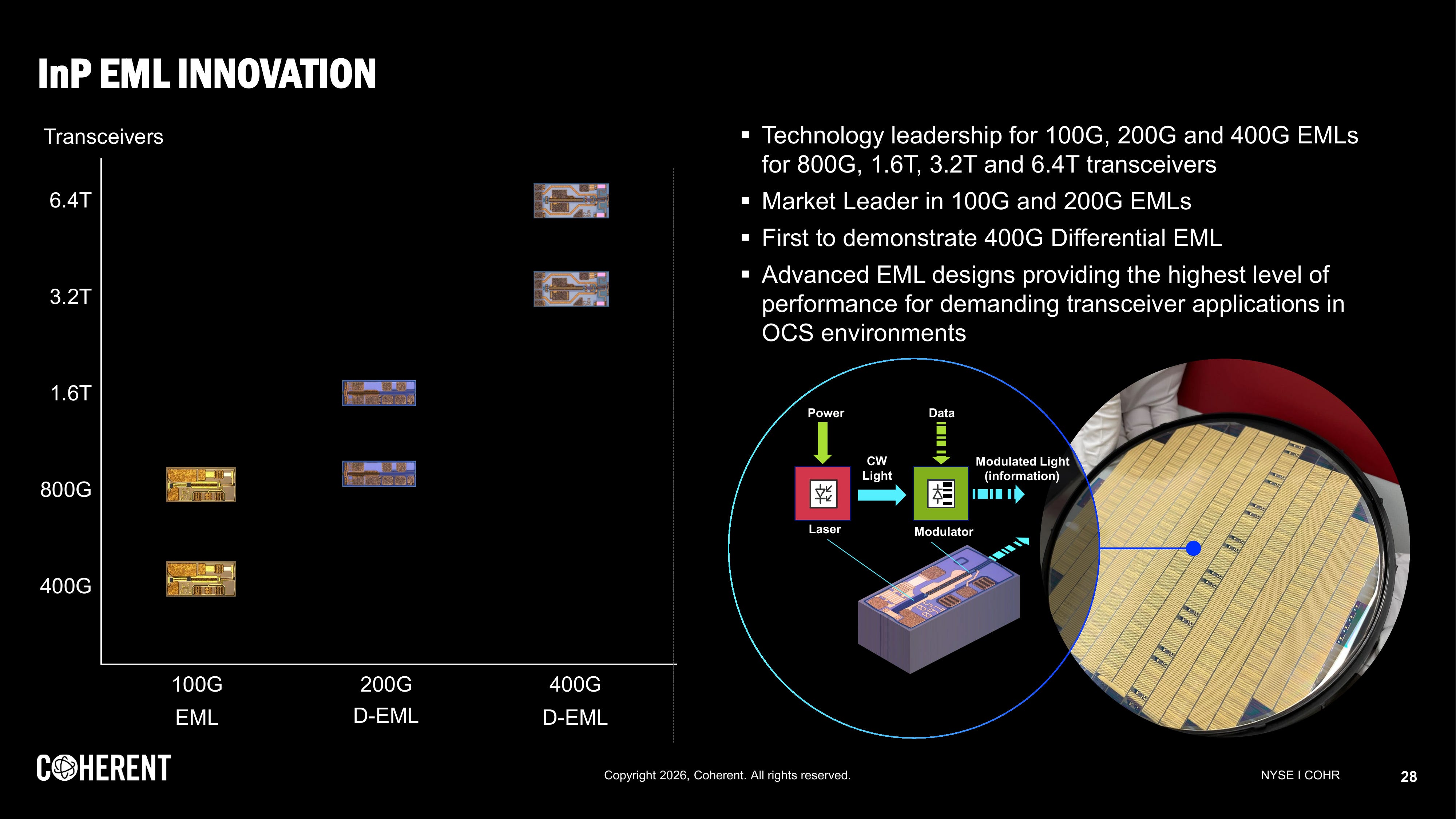

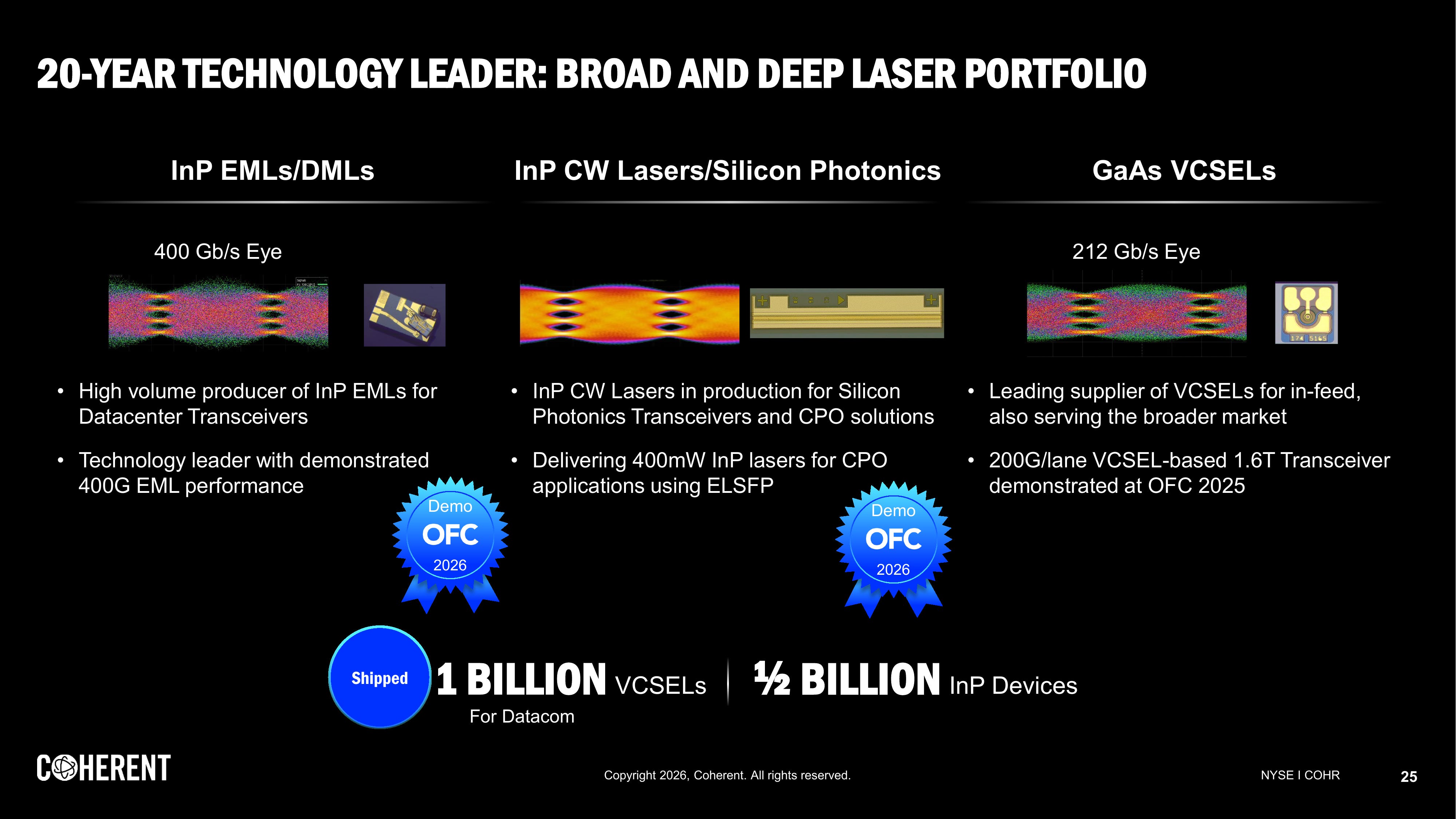

On EML laser chips, Coherent manufactures 100G EMLs for 400G and 800G transceivers, 200G EMLs for 800G and 1.6T, and demonstrated a 400G Differential EML for 3.2T and 6.4T at OFC 2026.

Coherent currently uses a mix of internal and external laser sourcing. Anderson confirmed at the Morgan Stanley conference that Lumentum is both a customer and a supplier, suggesting that Coherent’s internal EML capability has not fully displaced external supply across all performance tiers. The 6-inch cost advantage may be closing the gap, but the performance comparison against Lumentum’s epitaxy is still playing out.

For CW lasers, which power silicon photonics transceivers and are critical for co-packaged optics, Coherent is in full production and ramping on 6-inch InP in Sherman. At OFC 2026, it showed a 400mW high-power version for CPO applications.

CW lasers are one of the key product families covered by the Nvidia supply agreement. On the OFC status update call, Beck Mason (EVP Semiconductor Devices) set out to reassure everyone that CW laser yields on 6-inch wafers are looking promising:

BM: We’re currently running three main categories of devices on 6-inch indium phosphide, EMLs, high-power CW lasers and high-speed photodetectors. And

all three of those categories, we’re seeing higher yield and better throughput efficiency on our 6-inch lines than we’ve been able to achieve even on our very mature 3-inch production lines.

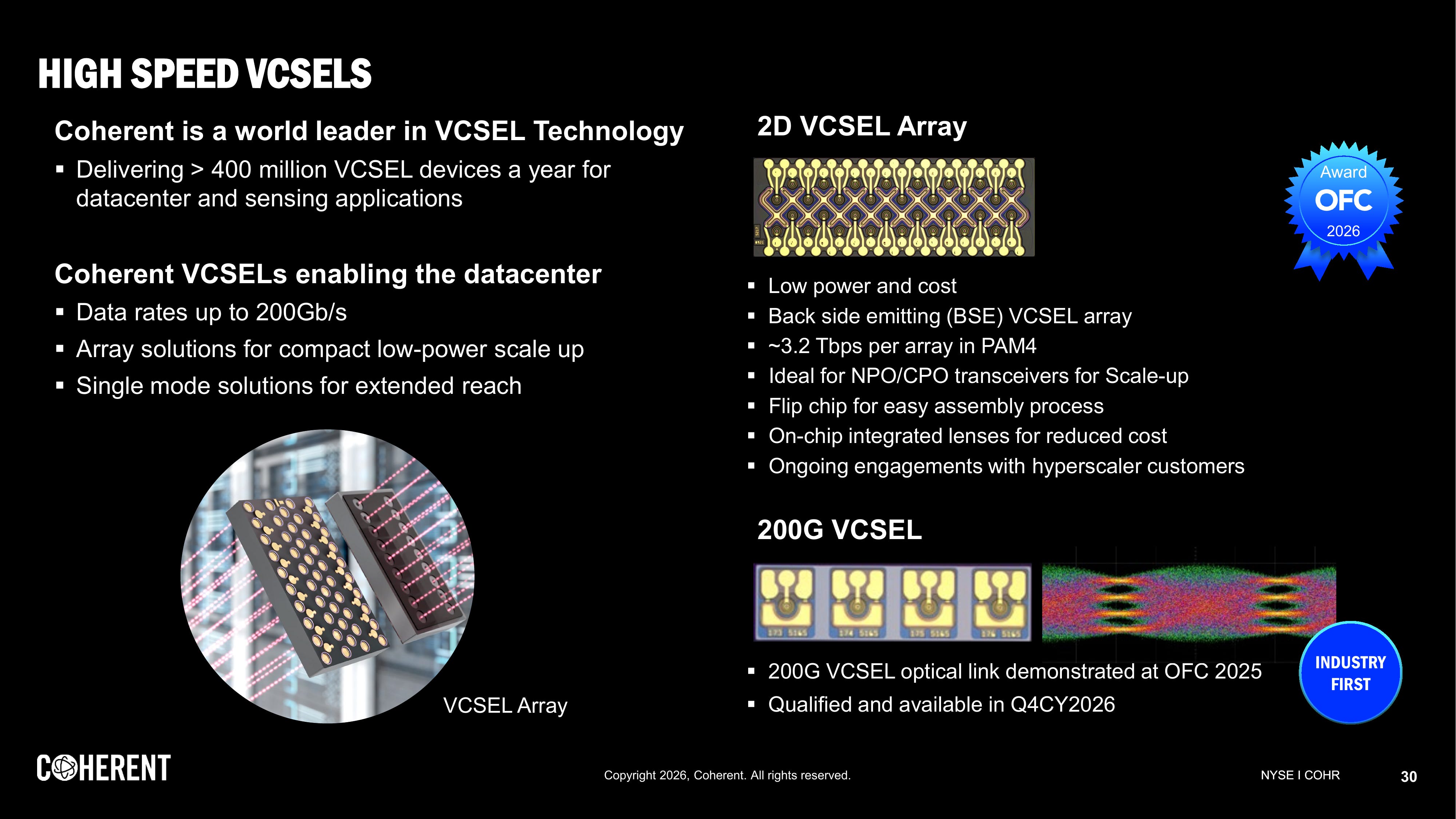

On VCSELs, Coherent manufactures GaAs-based vertical-cavity surface-emitting lasers. These serve Apple under a new multiyear 3D sensing agreement, and Coherent plans to launch a VCSEL-based 1.6T transceiver in the second half of calendar 2026.

VCSELs are a lower-power alternative to InP-based solutions, but with shorter reach. CTO Julie Eng explained the tradeoff at the OFC briefing:

“The VCSEL actually is an interesting potential for silicon photonics because the power is very, very low… it’s basically between 4x and 5x lower power than the silicon photonics solution. But it doesn’t go as far. It’s shorter reach.”

That means VCSELs could be used for in-rack and near-rack scale-up, where power and density are prioritized over distance, typically under 100 meters on multimode fiber.

Management says Coherent has ample gallium arsenide capacity, which is relevant because GaAs circumvents the industrywide InP bottleneck. Anderson expects VCSELs and InP-based approaches to coexist rather than compete:

“In the VCSEL-based solution, you usually have the laser in it. And so there’s some pluses and minuses of that. But I do think that these will coexist in CPO/NPO just as they have in pluggable transceivers.”

Coherent also has its own silicon photonics PIC platform and demonstrated a 400G pure silicon PN-junction Mach-Zehnder Modulator at OFC 2026. This is a pathway to 3.2T transceivers via silicon photonics rather than InP, giving Coherent optionality across both technology approaches.

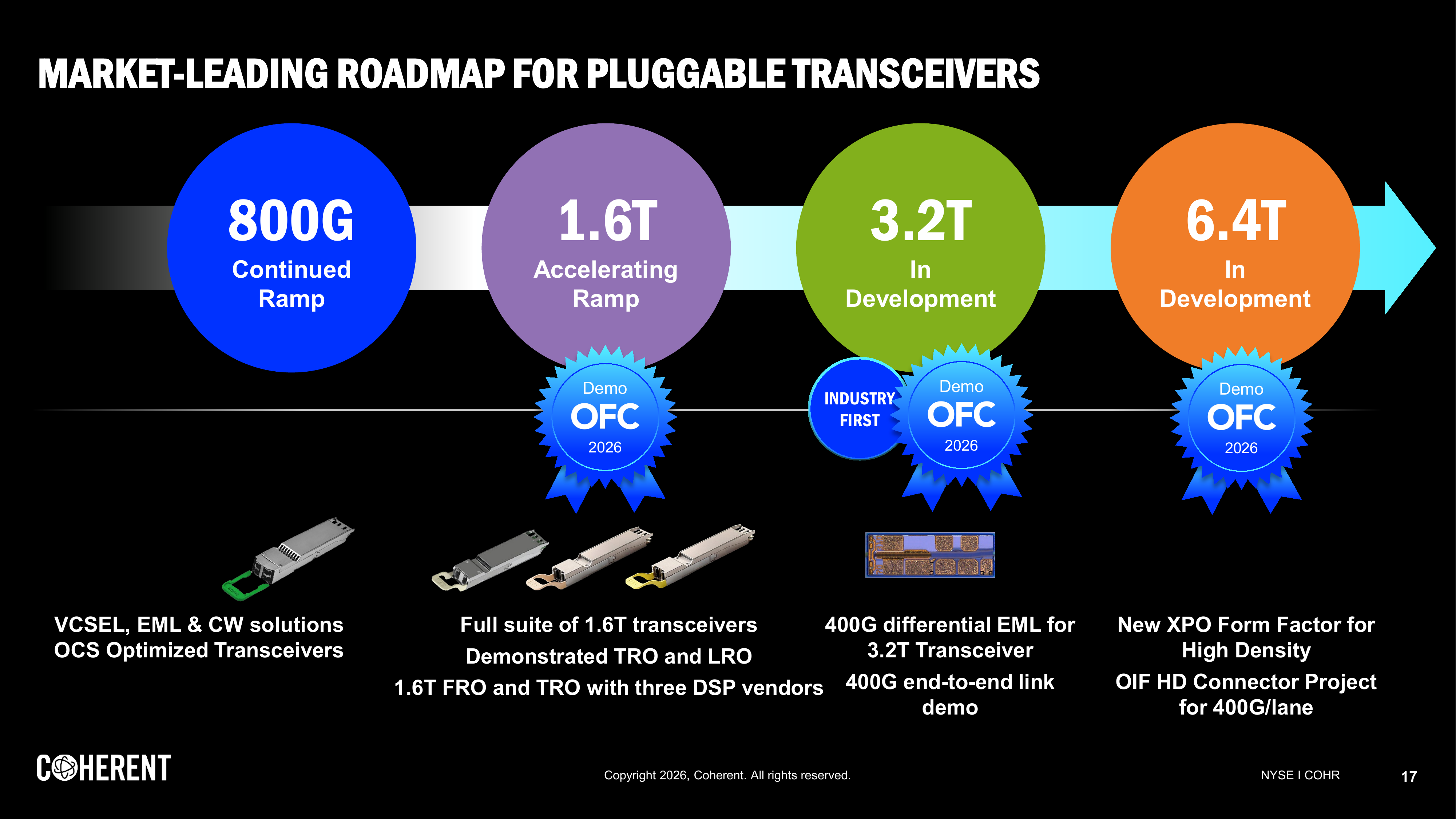

At the transceiver module level, Coherent ships full OSFP modules at 800G and 1.6T. At OFC, it showed 1.6T transceivers built with three different DSP solutions from three different industry leaders. That is notable because it positions Coherent as technology-agnostic at the DSP layer, in contrast to Broadcom, which makes its own DSPs and can offer a vertically integrated laser-plus-DSP package. Coherent is effectively saying it will work with any DSP partner, giving hyperscalers flexibility to choose.

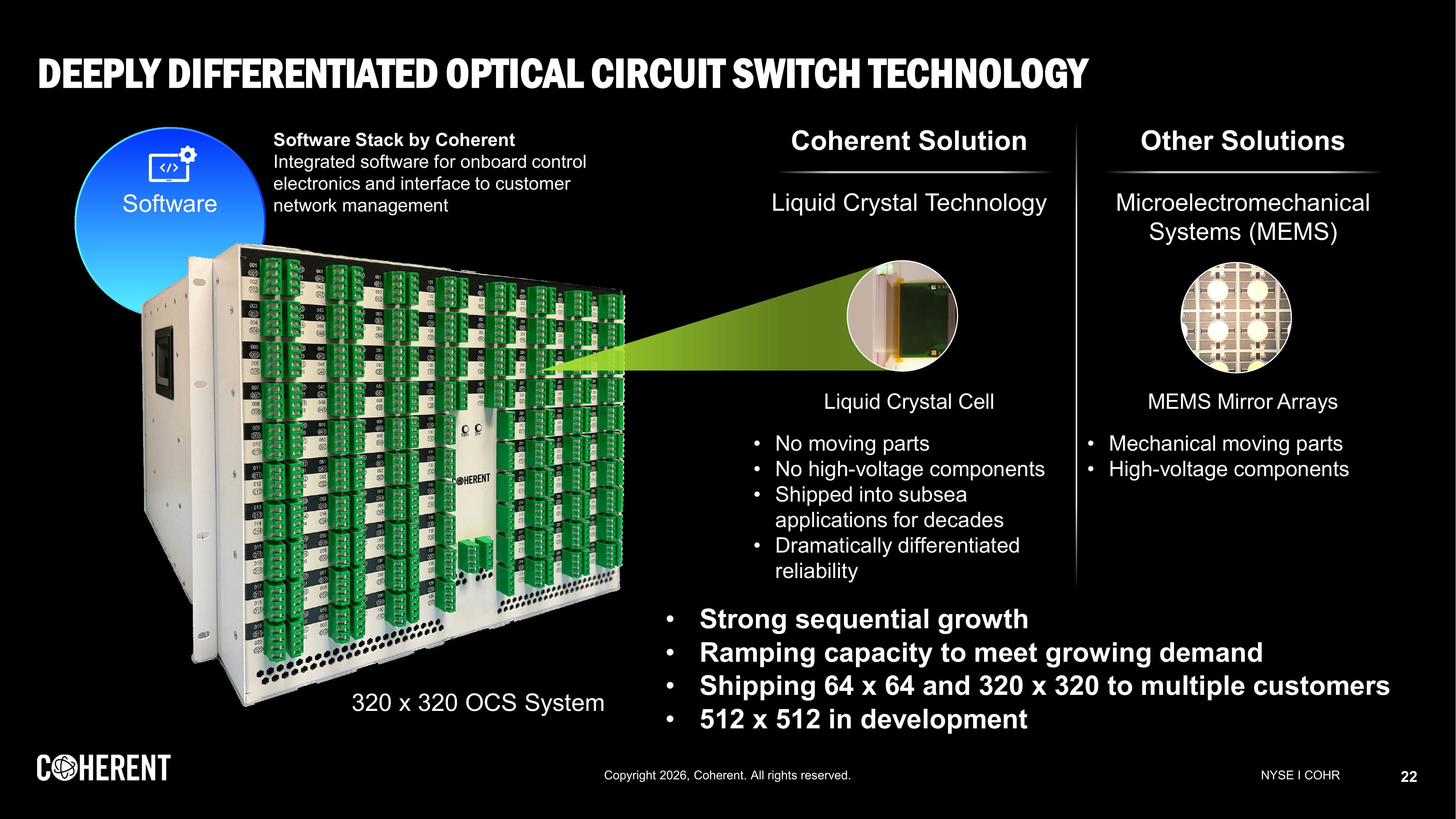

Beyond transceivers, Coherent makes optical circuit switches (OCS) using digital liquid crystal technology, which is non-mechanical and has no moving parts.

Anderson said at Morgan Stanley that Coherent is engaged with over 10 customers and that “multiple customers have already deployed in real data center applications”. Revenue shipments began in Q4 FY2025. This is a different technology from Lumentum’s MEMS-based OCS, and the two approaches are competing for the same emerging market.

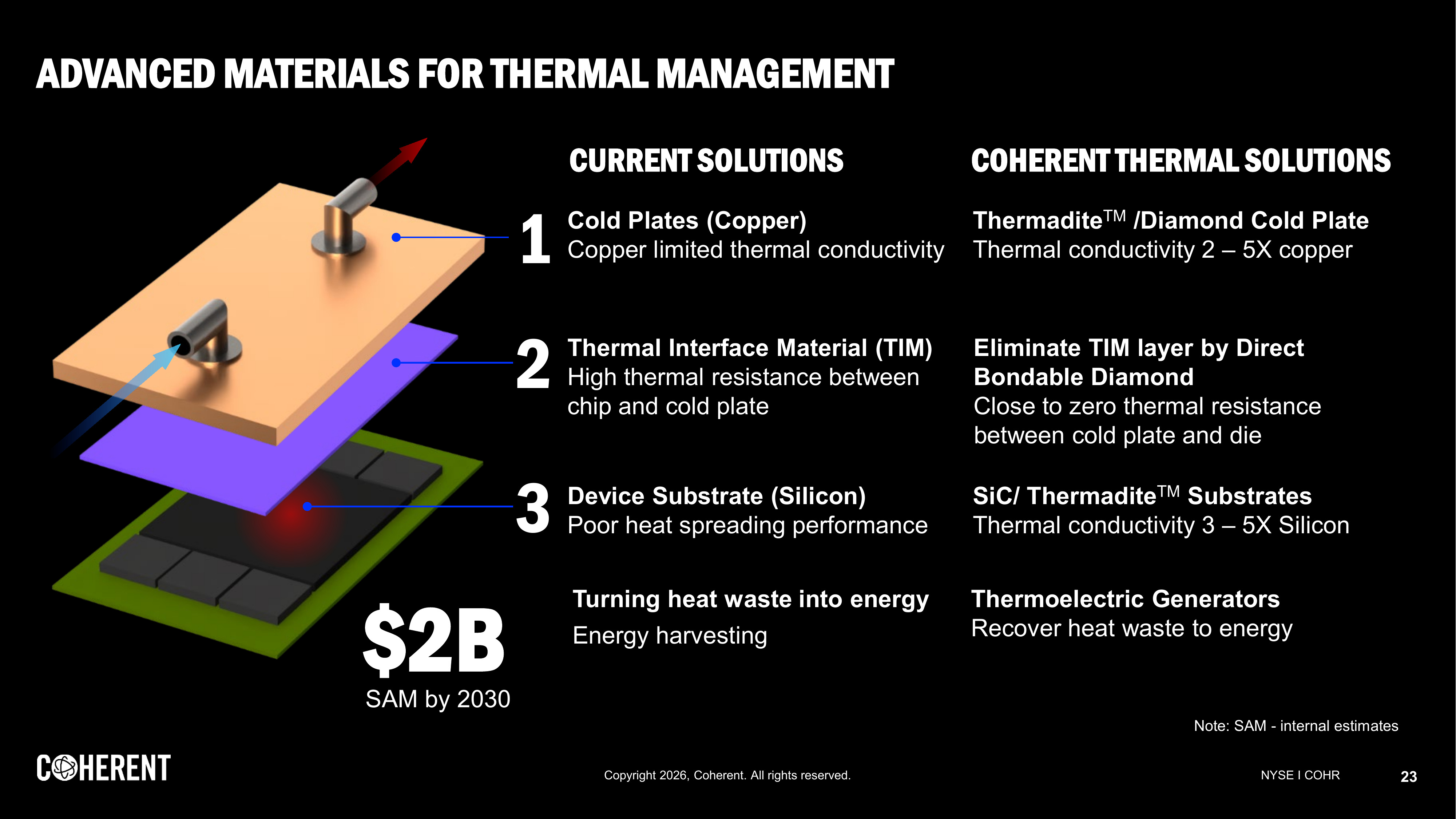

Finally, on the industrial side, Coherent has some interesting datacenter-adjacent materials. Thermadite is a proprietary material with what management describes as exceptional heat-transfer characteristics, which is being evaluated by large customers as a replacement for copper heat sinks in data centers. Coherent also has a thermoelectric material that can convert waste heat back into electricity.

Both are early-stage, but Anderson highlighted them at Morgan Stanley as longer-term growth opportunities that bridge industrial materials expertise with datacenter demand.

The bull case for all of this vertical integration is greater internal control over cost, supply, and iteration speed. Customers value having a single partner that can build EML-based, VCSEL-based, or silicon-photonics-based solutions, depending on the application.

Plus supply chain resilience across 60-plus manufacturing sites in 14 countries, more than 20 of which are in the United States (Q3 FY25 transcript).

JA: But the other -- the second point I would make in terms of supply chain resiliency is around vertical integration. And this applies to not just our data center business, but also to our industrial business, for instance, our laser business is if you look at a lot of the very key technology in feeds for whether it’s a data center transceiver or an industrial laser, we make ourselves, manufacture ourselves a lot of the very key components that go into our transceivers or laser systems or other products. And so that’s an important part of our supply chain resiliency and flexibility. So to the extent that there are changes in the landscape, the tariff landscape and to the extent we need to adapt manufacturing, move manufacturing to different places for the benefit of our customers, we certainly feel like we’ve got a very good, resilient, adaptable supply chain to leverage.

The bear case is essentially “doing everything means doing nothing best”. Lumentum’s epitaxy appears to be ahead (Coherent still sources some lasers externally). Broadcom’s system integration is deeper (laser plus DSP plus switch on-package). The risk is that Coherent ends up as a jack of all trades competing against specialists at every layer.

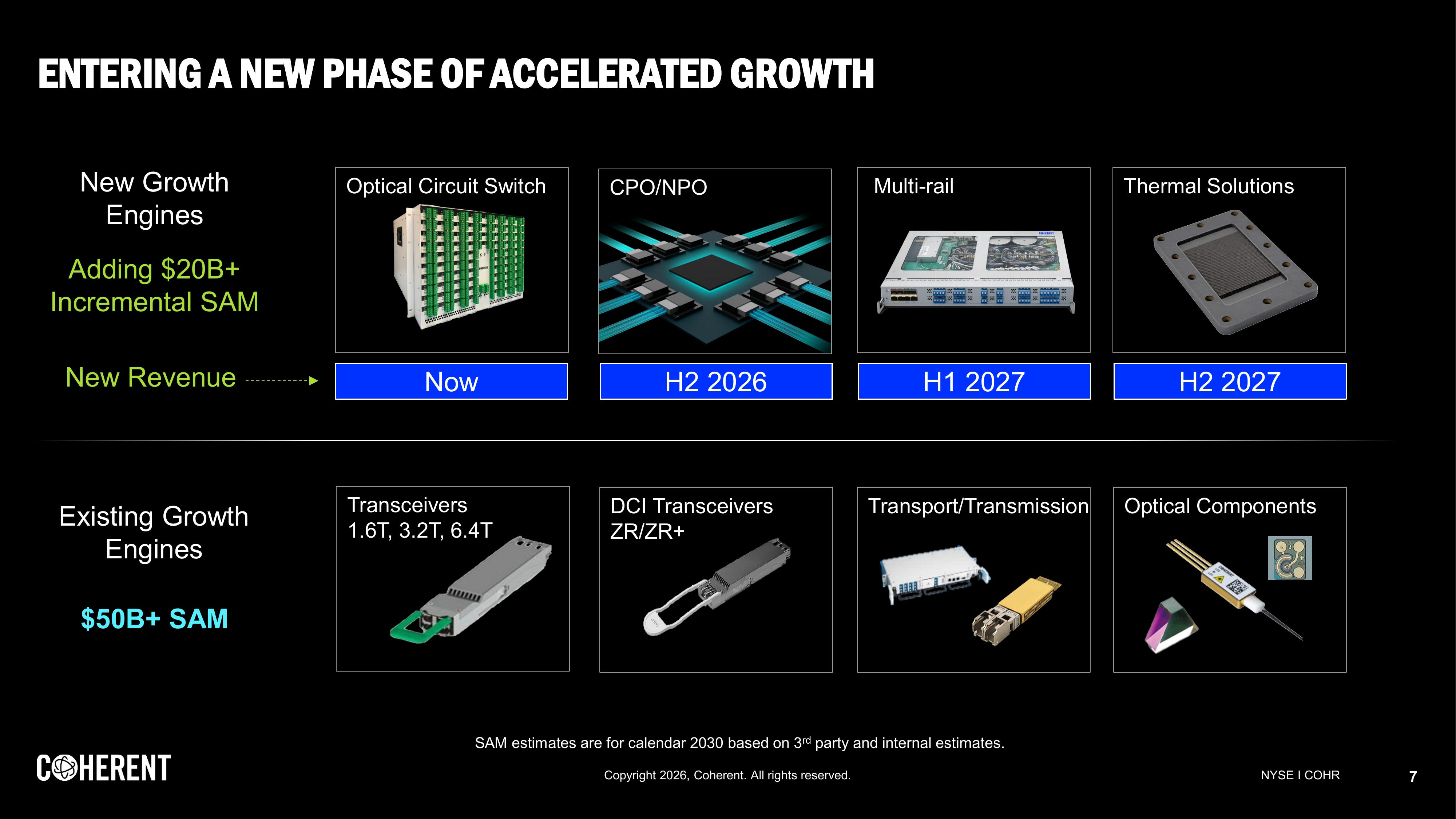

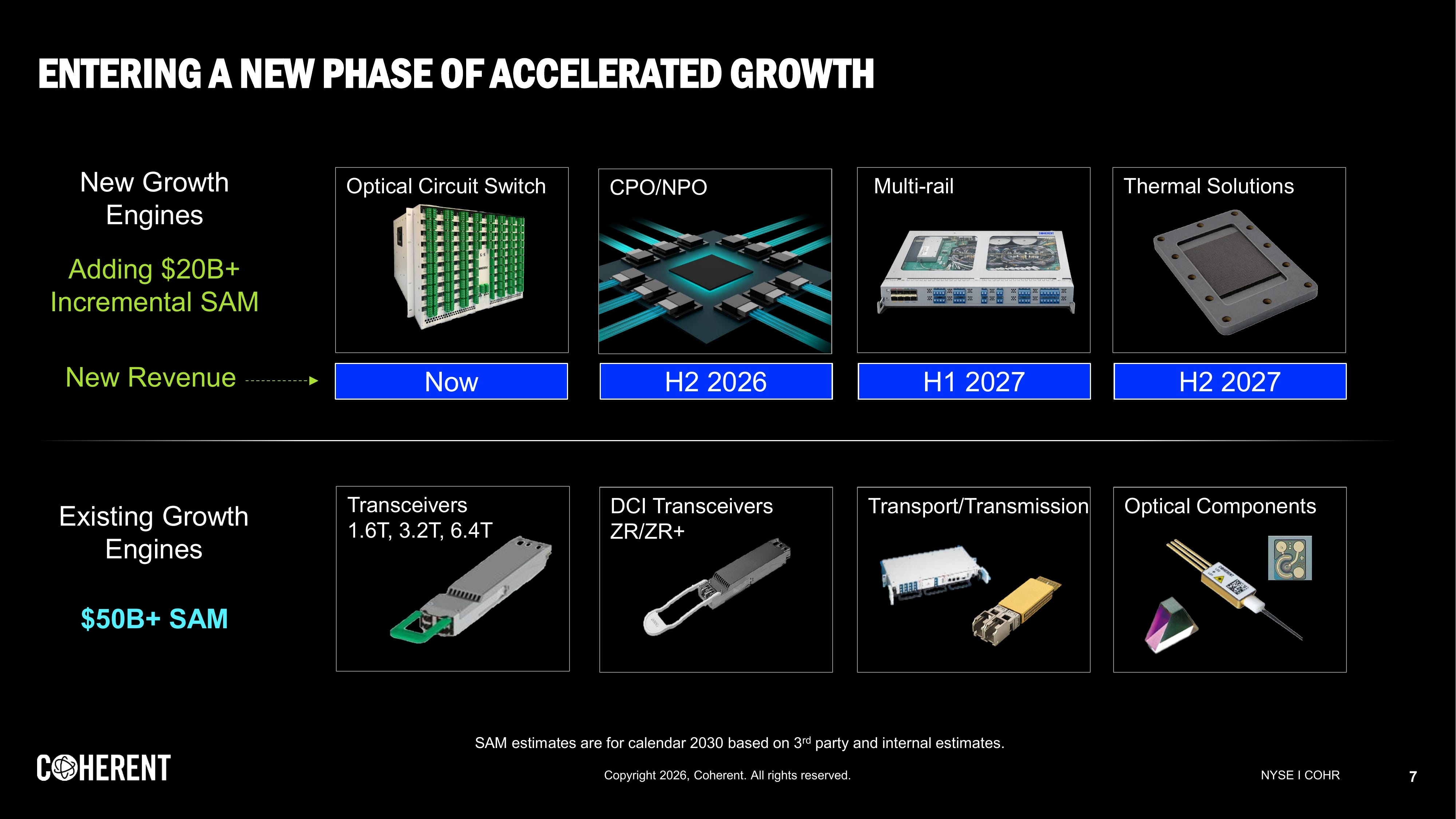

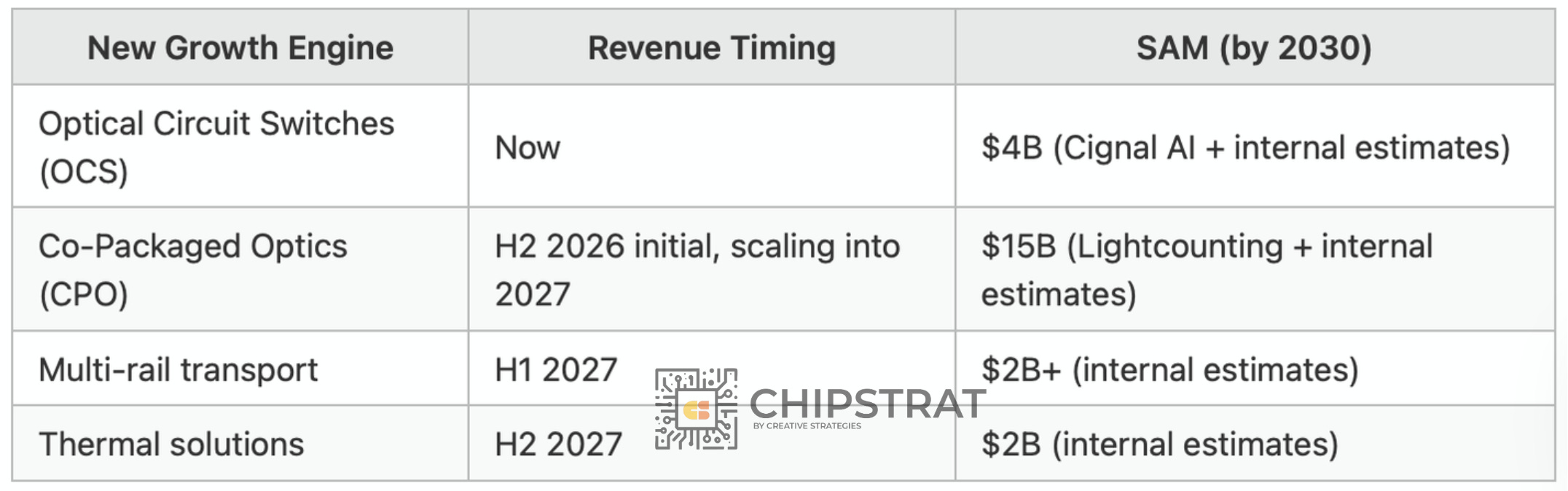

Growth Vectors

Coherent frames its growth story in two layers. The existing engines, pluggable transceivers (800G through 3.2T), DCI coherent transceivers, transport/transmission equipment, and optical components, collectively address a $50 billion-plus SAM per management’s estimates. These are shipping now and growing.

On top of that base, Coherent identifies four new growth engines that add over $20 billion in incremental SAM by 2030:

The stacking of these new engines on top of an already-growing base is why management says CY2026 is mostly booked, CY2027 is “filling very, very quickly,” and FY2027 revenue growth will exceed FY2026. Each new engine is at a different stage of maturity, so inflection points are spread over the next 18 months rather than concentrated in a single quarter.

Open Questions

So… Coherent has a very broad photonics stack with promising growth vectors at various stages of inflection. The stock has run from $45 to $250. The sell-side is overwhelmingly bullish.

Yet Coherent still sources some lasers externally, including from Lumentum. Broadcom has the full-stack CPO lead, even if its CEO says CPO is “not anytime soon.” Chinese module makers are winning volume at 800G. And the BIS Huawei investigation is still unresolved.

Which of these growth vectors holds up under scrutiny? Where is management credible and where are they hand-waving? How does Coherent stack up head-to-head against Lumentum and Broadcom across each product category?

I went through all of this against Q2 FY2026 earnings, the Morgan Stanley TMT Conference (March 3), OFC 2026 announcements, and sell-side research, then put together a three-way comparison with Lumentum and Broadcom.

Here’s what’s behind the paywall:

COHR vs. LITE vs. AVGO: Head-to-head across every product category

Six things to watch, each with a bull case, bear case, and what to look for next: the 6-inch InP bet, OCS liquid crystal vs. MEMS, CPO positioning, the margin path to 42%, BIS risk, and valuation

How the latest quarter stacks up against each of those

What the Street is saying and where analysts disagree

Catalysts for the rest of CY2026 and into CY2027

and more!