Lumentum and the Laser Bottleneck

Lumentum is winning and still can't keep up. Coherent is closing in. Earnings, sell-side sentiment, and the tensions to track.

There are so many bottlenecks in the AI cluster value chain. GPUs. CoWoS. HBM. And today, our focus is on another one: lasers.

Electro-absorption modulated lasers (EMLs) are the component inside optical transceivers that converts electrical data into light. It’s a laser and a high-speed modulator on a single indium phosphide chip, and every 800G and 1.6T transceiver needs them.

Lumentum makes more of these lasers than anyone, somewhere between 50-60% of the global market. Yet demand outstrips supply by roughly 30%!

Lumentum CEO Michael Hurlston said as much on the Q2 earnings call:

“We’re undershipping our customers’ demand by somewhere around 30%. Even as we’ve added 20% additional capacity, the demand-supply imbalance has increased.”

Dang. All EML capacity is locked under long-term agreements through calendar 2027. Customers coming back for more than their LTAs cover are paying premium prices. Customers who won’t sign LTAs risk losing supply priority entirely. Must be nice!

As CFO Wajid Ali said,

the LTA structure is “allowing us to have incremental pricing discussions around those incremental units.”

Of course, this pricing power is showing up in the financials. Revenue hit $665M, up 65% YoY, with $805M guided next quarter. Operating margins went from 7.5% to 25.2% in twelve months, and 30%+ guided next quarter. Whew!

Yeah, that explains why the stock trades at more than 60x forward earnings, and the current price has run ahead of the average sell-side target.

But bottlenecks and winning like this encourage competition.

The question thus is how long this temporary advantage holds, and whether the stock already prices in the answer. NFA, DYDD.

To get there, we first need to understand why the entire AI data center is going optical, and then why the laser layer is a bottleneck.

Why the Data Center Is Going Optical

Three shifts are expanding the optical TAM.

First, scale-out networking at 800G and above is increasingly optical. At 100G-per-lane speeds, copper alternatives like Credo’s AECs still work for short reaches (up to ~5-7 meters) and ALCs could push that to 30 meters. But anything beyond that requires optical transceivers, and each one needs EML laser chips. As lane speeds jump to 200G for 1.6T, copper reach compresses further, expanding the optical TAM with every speed generation.

Second, scale-up is going optical. Copper has dominated inside-the-rack connectivity (NVLink), but it’s hitting a physical wall at higher speeds. The industry is actively exploring alternatives. Nvidia demonstrated die-to-die optics at ISSCC in February using TSMC’s COUPE 3D hybrid bonding platform with silicon photonics engines. Marvell acquired Celestial AI for its photonic fabric technology. Ayar Labs (backed by Intel and Nvidia) is building optical I/O chiplets for in-package chip-to-chip communication. Broadcom’s ESUN spec targets Ethernet-based optical scale-up. Even Credo, the copper champion, is hedging with ALCs that use micro-LED light sources for row-scale scale-up.

This creates an entirely new optical TAM that didn’t exist two years ago. Lumentum CEO Hurlston on the Q2 call:

“Copper has long been the gold standard for scale-up... it is hitting a physical wall. An industry pivot is underway. By late calendar 2027, we would expect our first scale-up CPO shipments, replacing longer copper connections.”

One note: I see folks conflating Nvidia’s CPO announcements with scale-up. Nvidia’s current CPO switches (Quantum-X Photonics, Spectrum-X Photonics) are on the scale-out fabric, not scale-up. NVLink remains copper today. Optical scale up is a transition that’s just in its infancy.

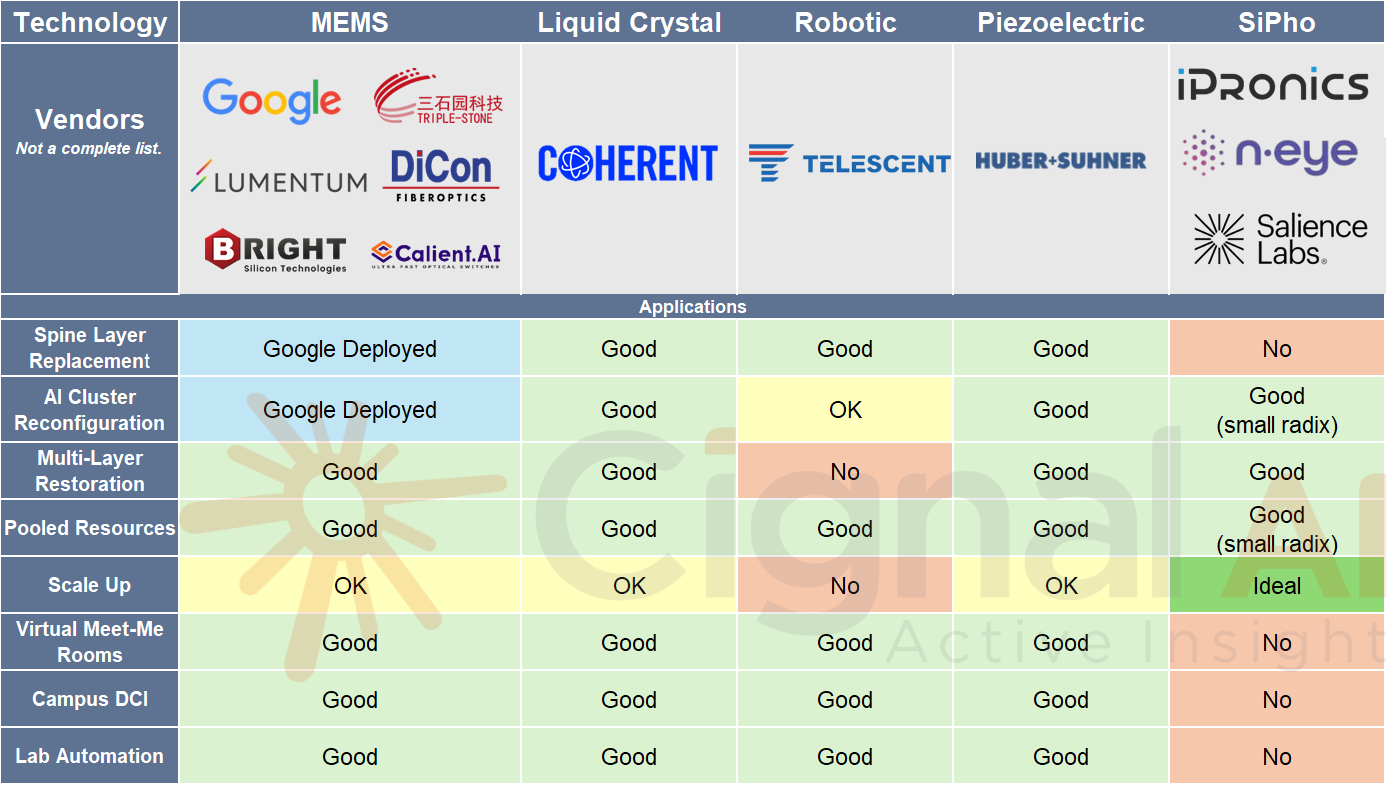

Third, Optical Circuit Switching is a new category. OCS reconfigures optical paths in milliseconds, replacing fixed electrical spine switches. Google pioneered this for AI cluster networking. I think this technology is awesome; it’s lower-power because it stays in the optical domain, so there's no need to convert light into electrical signals for switching and routing.

Google historically built its own, but the technology is moving to merchant vendors. Lumentum’s OCS backlog went from zero to over $400 million in roughly a year. Three customers, four use cases (spine replacement, scale-across, scale-up, redundancy). Cignal AI projects the OCS market will exceed $2.5 billion by 2029.

Lumentum’s approach uses MEMS-based mirrors:

So Where Does Lumentum Stand?

Lumentum is a great spot, with three expanding optical TAMs (scale-out, scale-up, and OCS) and shipping lasers into all of them.

And icing on the cake, just today Nvidia invested $2 billion in both Lumentum and Coherent today, with multibillion-dollar purchase commitments for future capacity. See NVIDIA Announces Strategic Partnership With Lumentum to Develop State-of-the-Art Optics Technology

As we said, bottlenecks attract competition though. Coherent is ramping 6-inch indium phosphide wafers, which could yield 4x as many dies per wafer at significantly lower cost. Tower and GlobalFoundries are 5Xing SiPho capacity, which could eventually route around EML-based transceivers entirely. Mesh Optical Technologies, a startup founded by SpaceX alumni, raised $50M to build 1.6T transceivers using semiconductor-style packaging instead of traditional manual optical assembly. The typical big claims from a new startup, but an interesting point to watch because it would simultanesouly increase capacity and decrease cost.

The nearest-term capacity risk is Coherent. If Coherent’s 6-inch yields truly close the gap with Lumentum’s 3-inch performance (as they claim), the scarcity that drives Lumentum’s pricing power will end. There’s still a side-by-side performance comparison to make at that point, not to mention future generation laser supply constraints. Whoever can get there first can enjoy the same pricing dynamics.

I broke Lumentum’s story into some clear points of tension to track, and scored each against Q2 FY2026 earnings and sell-side research.

Here’s what’s behind the paywall:

Lumentum’s business units: the component and systems businesses, the epitaxy moat, and why even competitors buy LITE’s lasers

Four Growth Vectors: EML, OCS, CPO, and optical scale-up. What’s shipping now, what inflects in H2 2026, and what’s a 2027+ story

Tensions: bull vs. bear on the EML moat, OCS market creation, CPO timing, supply chain risk

Sell-Side Sentiment: what the Street is saying and where analysts disagree

Earnings Scorecard: each tension scored against Q2 results, management quotes, and sell-side evidence