VCSELs + 200G Wall In AI Datacenters?

Decades of short-reach dominance, the supply chain holding it up today, and the problems at the 200G transition

Coherent has lately been talking about parallel-pathing the light source for 1.6T transceivers, developing solutions based on SiPh (silicon photonics), EMLs (electro-absorption-modulated lasers), and VCSELs (vertical-cavity surface-emitting lasers). From the recent earnings call:

CEO Jim Anderson: A significant portion of the sequential growth we expect in the current quarter is driven by 1.6T adoption. As a reminder, earlier this year at OFC, we were the only company to demonstrate 3 different types of 1.6T transceivers based on 3 different types of laser sources; silicon photonics, EML and VCSEL.

My “pay attention” radar went off when I read this. Why all three? Are they hedging bets here? Which bet is better? What are competitors betting on? Feels like a tech inflection opportunity that could shake up industry and market dynamics. Will one or more of these fail?

Answering those questions first requires foundational knowledge in each technology and current market dynamics.

Let’s start with VCSELs for datacenter communications. We’ll start simple.

What is a VCSEL?

Why has it dominated the short reach data center market for decades

Why is the 200G-per-lane jump giving everyone heartburn?

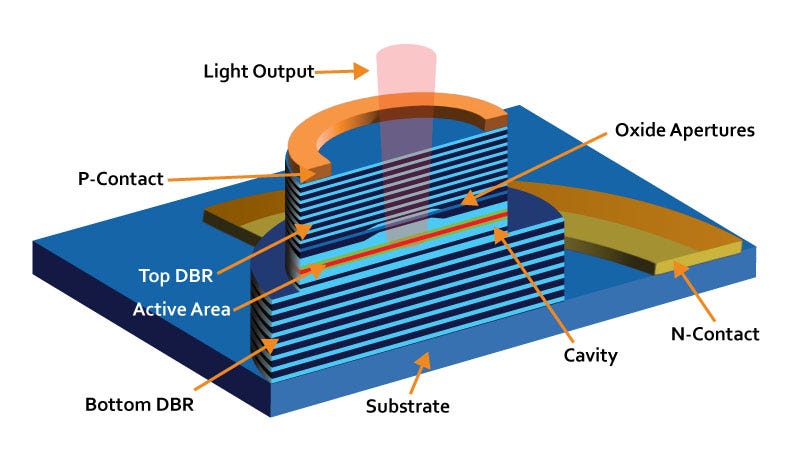

What Is a VCSEL?

VCSEL stands for Vertical-Cavity Surface-Emitting Laser. The “vertical” part is the giveaway. A VCSEL is a tiny semiconductor laser that fires light straight up out of the top of the chip:

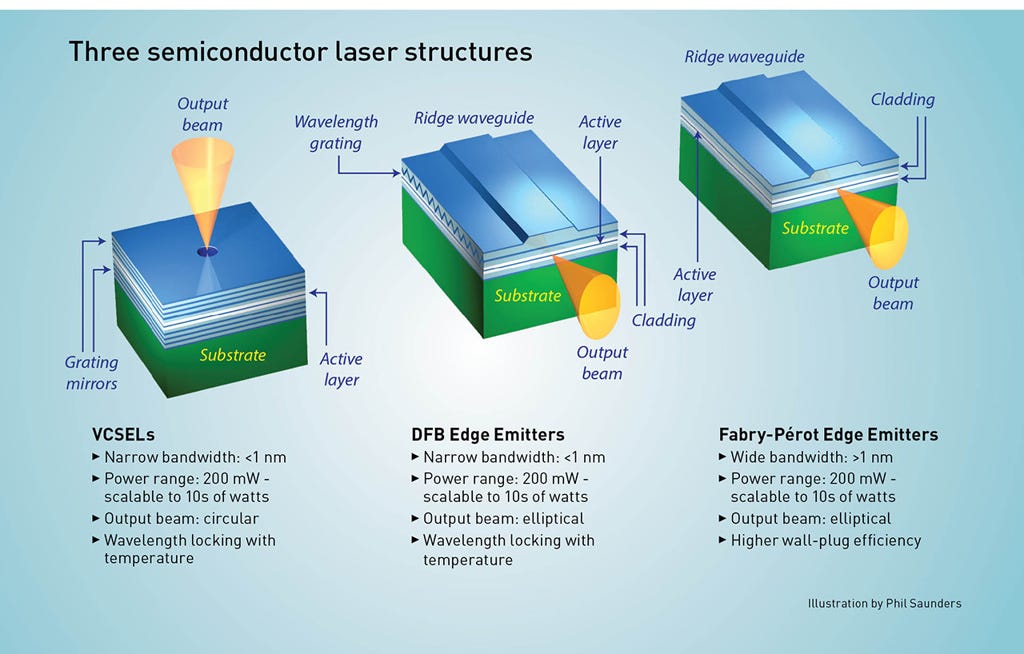

This contrasts with edge emitters, which emit light from the edge of the laser:

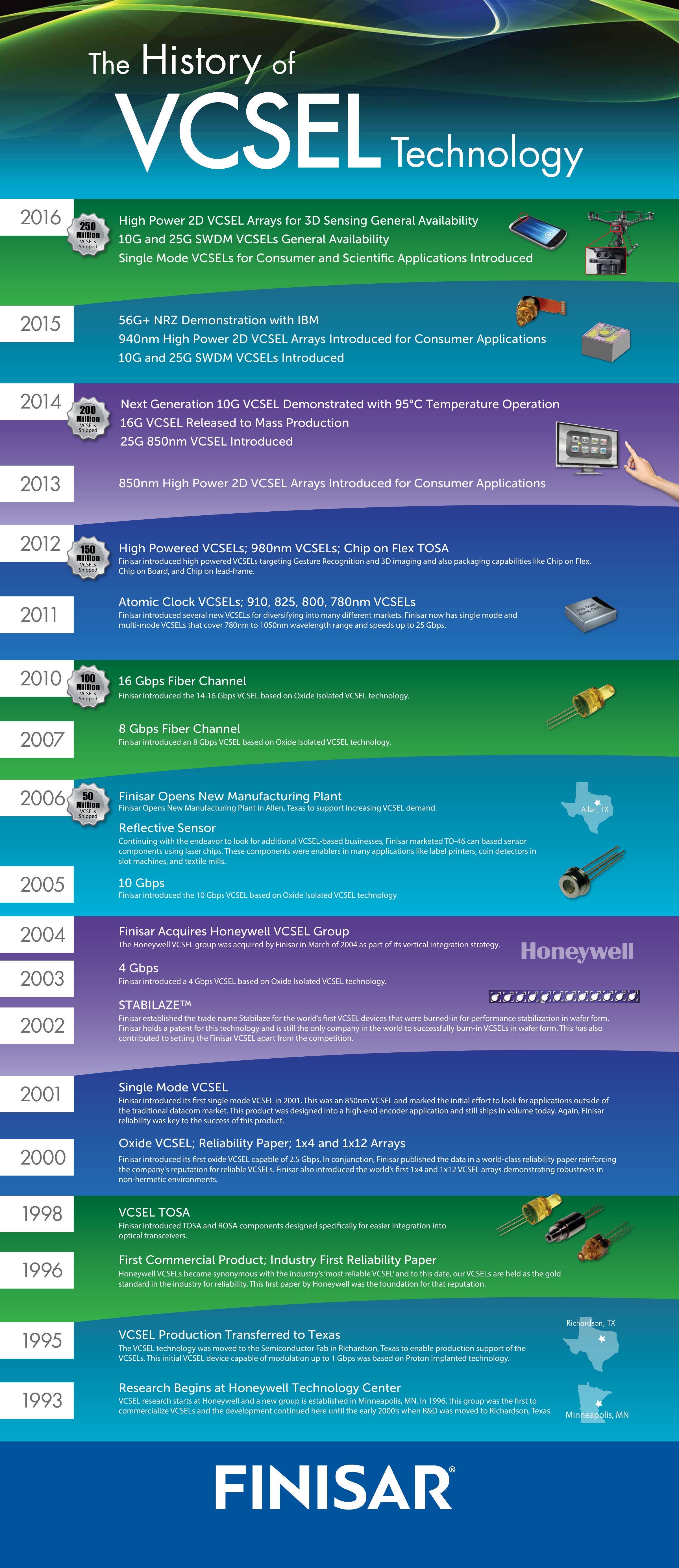

Honeywell began VCSEL research in 1993 in Minneapolis, moved it down to Richardson TX in 1995, and launched the first commercial product in 1996, initially targeted for datacenter communications. The history is a fun chain of acquisitions: Finisar acquired Honeywell’s VCSEL Group for $75M in 2004 (what a steal), II-VI acquired Finisar in 2018, and then II-VI acquired Coherent Inc. in 2022 and renamed the resulting entity Coherent Corp. So when Coherent talks about VCSELs today, it is effectively the heir to the entire 30-year US VCSEL development arc!

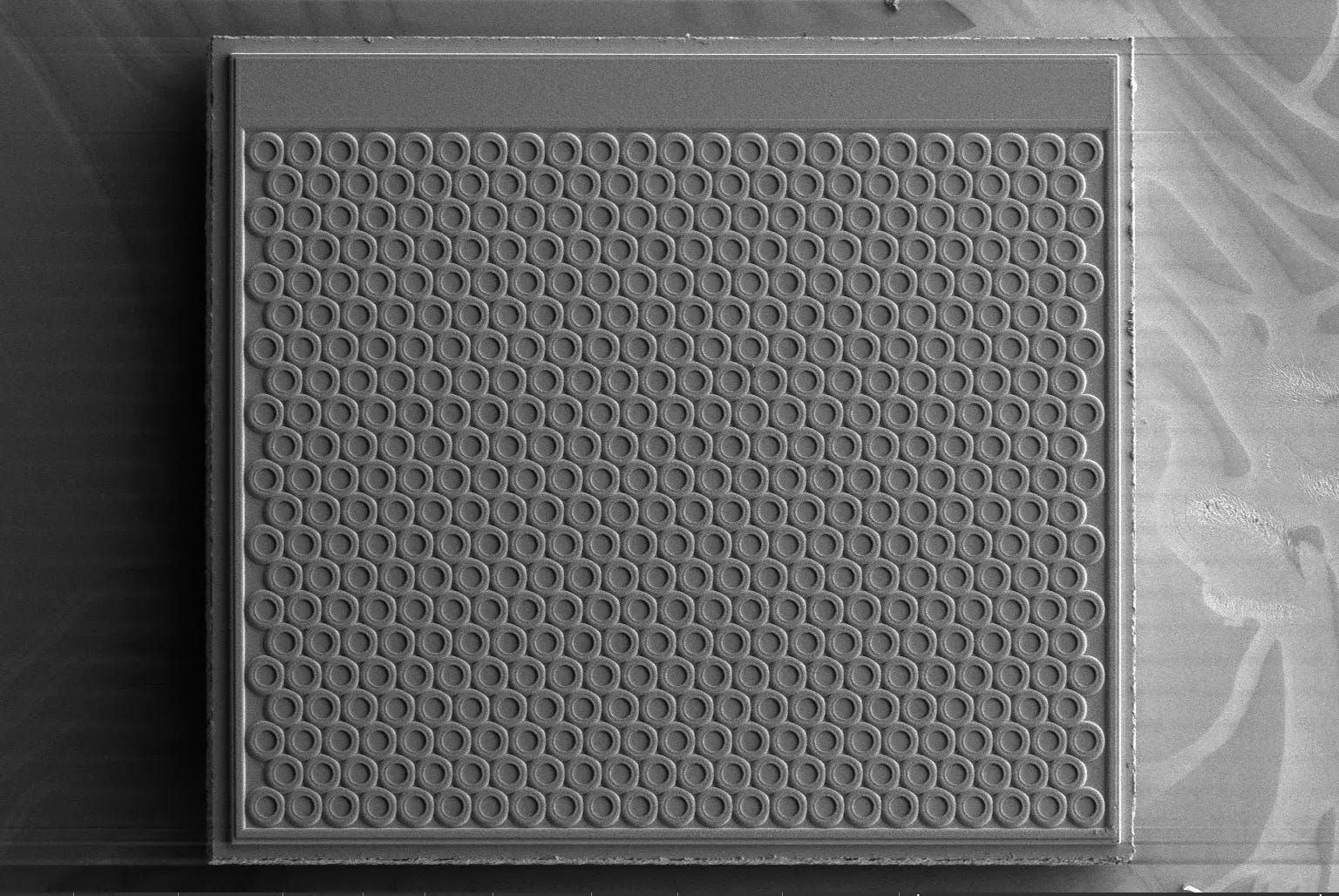

Check out this great infographic for more history. And note the volume of VCSELs shipped even a decade ago.

Commercial adoption was largely propelled by the Gigabit Ethernet (IEEE 802.3z) and Fibre Channel standards. VCSELs were a significant improvement over edge-emitting lasers in reliability, speed, cost, power efficiency, and manufacturability at similar wavelengths. For the first decade of existence, VCSELs were mostly used for short-reach datacom.

In 2017, high-power 2D VCSEL arrays were incorporated into the iPhone for Face ID, and consumer applications have since become the primary drivers of VCSEL production volume. Today VCSELs are everywhere:

Smartphone face ID and 3D sensing. When your phone unlocks by reading the geometry of your face, that’s a VCSEL array projecting structured infrared light at you.

Automotive LiDAR. VCSEL-based LiDAR is one of the architectures that self-driving systems use to build 3D maps of the world.

Optical mice and touchless sensors. The dot of light under your computer mouse is (very often) a VCSEL.

Short-range fiber communication and Active Optical Cables

ams OSRAM has a nice walkthrough of VCSEL technology for various applications, and their BELAGO 1.2 dot projector is a representative product.

As you know, below ~10 meters, copper cables still dominate but struggle as speeds increase:

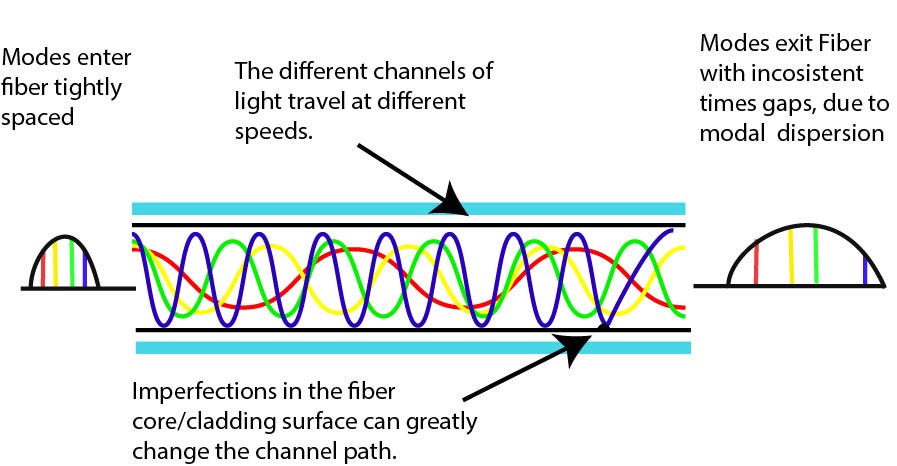

Beyond a certain distance, single-mode fiber takes over to avoid modal dispersion. That distance is data-rate-dependent and has been compressing rapidly, historically around 300 meters at 10G-era links, around 100 meters at 25G on OM4, and dropping to roughly 30-50 meters at 200G PAM4.

That middle slice (multimode fiber, between where copper gives up and where single-mode takes over) is VCSEL territory. Note that the slice itself is shrinking as data rates climb.

Another important note: What matters for the analysis later is that VCSELs have a very mature supply chain. Billions of VCSELs ship per year (mostly into consumer devices). The reasons VCSELs got pulled into all those applications is because VCSELs are compact, energy-efficient, array-friendly, wavelength-stable, and uniquely testable on-wafer before any packaging happens.

Why We Care About VCSELs Right Now

VCSELs are at an inflection point in 2026. AI data centers consume short-reach optical interconnect at a scale nothing in computing history has matched, and the industry is racing from 800G to 1.6T with 3.2T on the horizon. To get there, incumbents are trying to double each lane from 100G to 200G, and 200G is where the current path struggles. And how would it even double again to 400G/lane?

This post (the first in a series) will explain why VCSELs have dominated short-reach data center optics for two decades and what, specifically, is breaking at 200G.

We will cover:

The value props that built VCSEL’s moat at short reach plus wafer economics

What came before VCSELs, and why edge emitters still own long-haul

The named market players holding up today’s 800G/1.6T short-reach supply chain

Why the 200G-per-lane transition is breaking the moat