Hardware as a Differentiator: Block's Unique Approach to Financial Services

Hardware as a Core Competency, The "Apple Ethos" in Payments, Business Model, Ecosystems and Playbooks

Block is building a 3nm Bitcoin mining ASIC.

Huh? A financial company designing hardware on leading-edge process technology?

This news led me down a rabbit hole of research, and I’m sharing what I learned in a two-part series.

To grasp Block's Bitcoin strategy, we first need to understand Block’s core businesses and hardware strategy. Part one will provide this essential context, while part two will explore their specific Bitcoin endeavors.

Yes, this is a change of scenery from discussing the typical logic companies (Intel, Nvidia, Arm, etc). But it’s a fun intellectual exercise and a reminder that hardware can enable creative solutions for common issues in daily life.

And hey, we could all use a quick break from the Generative AI hype dominating semiconductors, right?

Who is Block?

Block is the parent company of several financial tech companies, including Square and Cash App.

From Block’s 10K,

On December 1, 2021, we changed our corporate name from Square, Inc. to Block, Inc. Block is the name for the company as a corporate entity. Since our start in 2009 with the Square business, we have added Cash App, TIDAL, and TBD as businesses. Our two reportable segments are Square, formerly referred to as Seller, and Cash App, which reflects our two primary ecosystems.

Note that Block houses many businesses but only reports the profits and losses of Square and Cash App. We’ll discuss the other businesses in depth later; for now, just know that TIDAL is a questionable acquisition and the other businesses are Bitcoin-related.

Block first began as the company Square.

Square

In The Beginning There Was Hardware

Square, created by Jim McKelvey and Twitter's Jack Dorsey in 2009, made it possible for anyone with a mobile device to accept all major credit cards.

The founding story traces back to a frustrated small business owner who happened to be an engineer too:

Early in his career, McKelvey used his glass-blowing skills — creating works like bowls and bathroom faucets — as an extra source of income and a way to offset lean years common to bootstrapped startups. In addition to supplementing his income, McKelvey’s glass-blowing business provided the inspiration for Square.

One day, McKelvey was venting to Dorsey about a $2,500 sale he lost because he was unable to accept an American Express card at his glass blowing studio. He was trying to sell a glass bathroom faucet to a woman in Panama, but he didn’t have the ability to accept payments other than cash, check, Visa and MasterCard.

It was a breakthrough moment for the pair, who recognized that all of the technology required to streamline payments for small businesses already existed. The parts had simply not been arranged correctly. McKelvey tackled the hardware, and Dorsey developed the software. By the end of 2009, Square was launched.

Square was launched to reimagine the physical payment experience. As explained in Square’s S1 filing ahead of their 2015 IPO,

We are driven by economic empowerment and work to democratize commerce—leveling the playing field for sellers of all sizes. Our focus on technology and design allows us to create products and services that are accessible, intuitive, and easy-to-use. We set attractive and transparent pricing that is easy for our sellers to understand. We provide a free software app with our affordable (often free) hardware to turn mobile devices into powerful POS solutions in minutes.

Square's commitment to a frictionless payment process led them to design their own hardware from from day one.

This mindset reminds me of the iPod's early days when Apple conceived a better portable music experience which required innovating with both hardware (iPod) and software (iTunes).

Like Apple, Square’s founders prioritized beautiful industrial design and seamless end-to-end user experiences for their initial product.

We can already see Square’s founders sharing an Apple ethos.

Let’s look a bit more into Square’s business and then we’ll dive deeper into their hardware.

Business

Today, Square supports many point-of-sale (POS) form factors beyond the phone, including handheld terminals, iPads, kiosks, and full-blown registers. I’m sure you’ve seen these at a local restaurant or coffee shop:

Ecosystem

Square has expanded beyond POS hardware into various software-enabled customer journeys.

We offer products and services for our sellers to start, run, and grow their businesses.

For employers, this includes capabilities like staff management tools, appointment scheduling, banking, e-commerce, and more. Square's focus isn't just on sellers; customers enjoy a range of advantages too, including a "buy now, pay later" service.

It’s should come as no surprise that Square expanded beyond the point of purchase. Square’s primary customers are micro and small-to-medium businesses (total annual receipts of <$1M) who are especially amenable to one-stop-shop software that’s easy to use and simplifies their already busy lives. No small business owner enjoys the pain and cost of cobbling together various point solutions to solve their problems. Square aims to solve as much of their pain as possible in a single seamless ecosystem.

These same micro and small business customers are often open to a better banking experience as well, which Square has also expanded to provide.

Square refers to its suite of financial offerings as a “commerce ecosystem.”

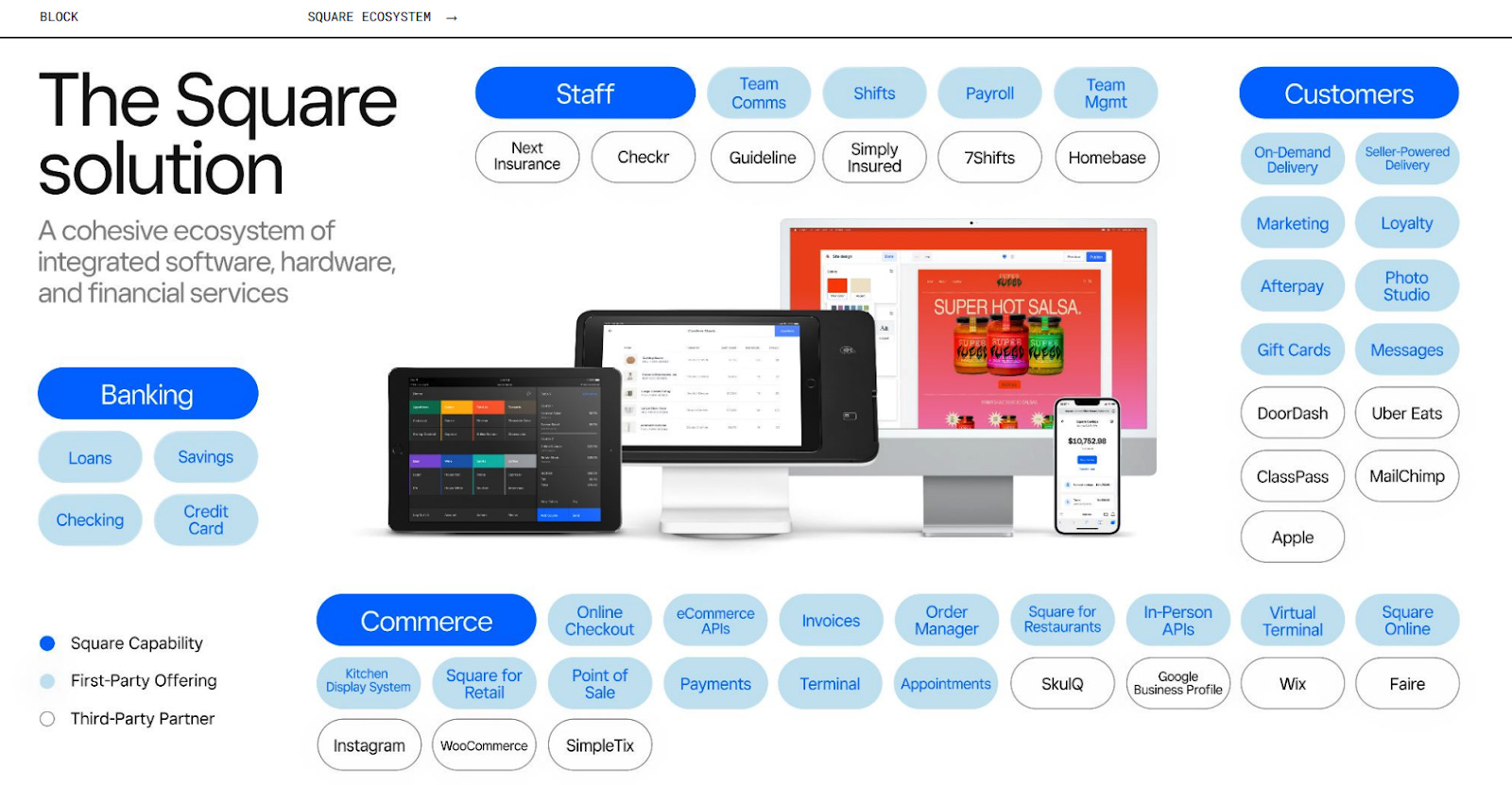

We have since expanded Square into a cohesive commerce ecosystem that provides more than 30 distinct products and services to help our sellers start, run, and grow their businesses. We combine software, hardware, and financial services to create products and services that are cohesive, fast, self-serve, and elegant. These attributes differentiate Square in a fragmented industry that traditionally forces sellers to stitch together products and services from multiple vendors, and often rely on inefficient non-digital processes and tools. Our ability to add new sellers efficiently, help them grow their business, and cross-sell our products and services has historically led to continued and sustained long-term growth.

Square’s ecosystem enables a digitally-native experience for entrepreneurs and businesses in the physical world—from Main Street mom-and-pop shops to large operations like SoFi Stadium, home of the NFL’s Rams and Chargers.

The core needs of retailers are the same: accept money from this buyer. Yet, the broader customer journeys can differ across retailers. Thus, Square's marketing strategy includes packaging its various products and services into industry-specific solutions, such as "Square for Retail" and “Square for Restaurants.”

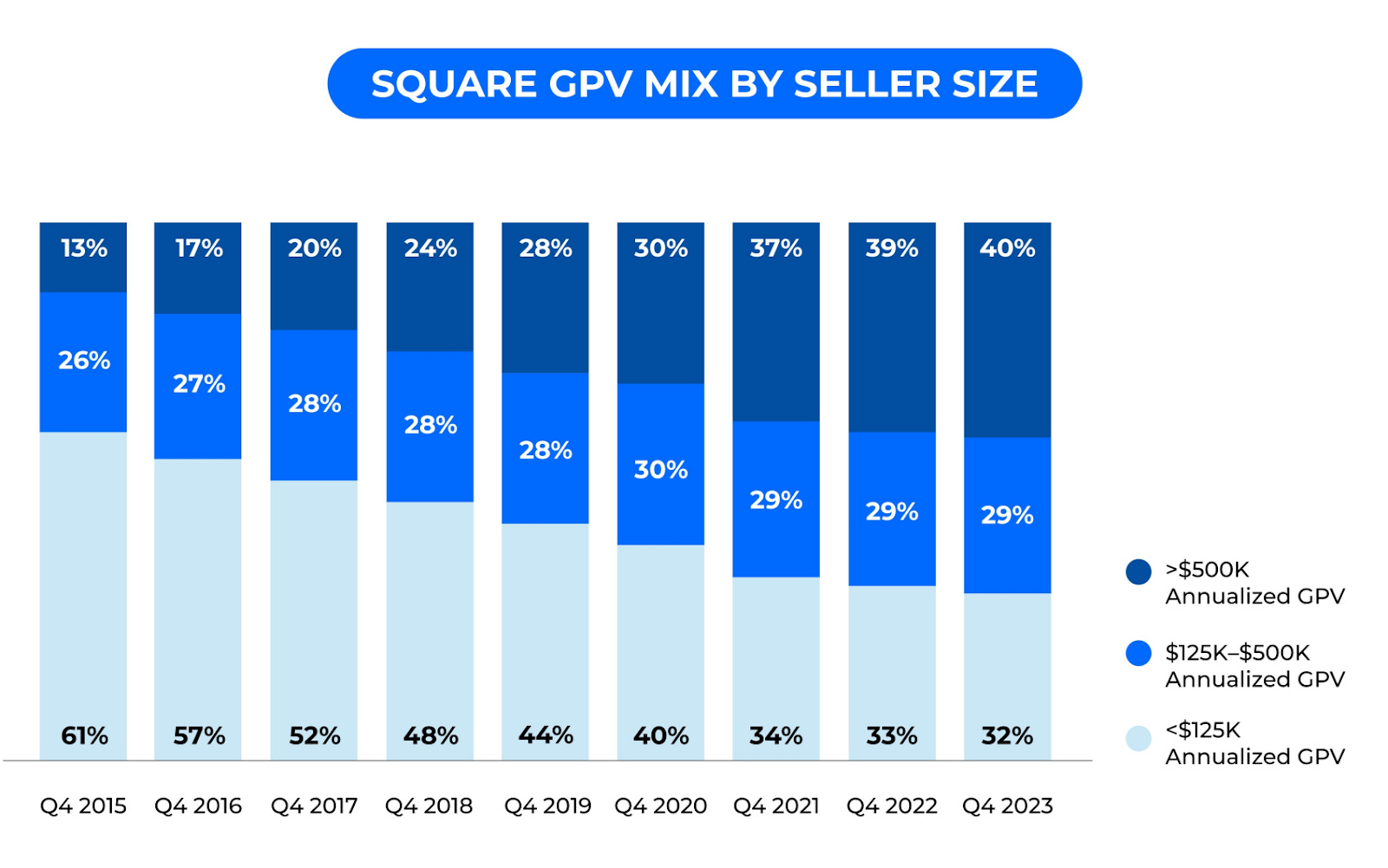

Moving Upmarket

Square is increasingly catering to larger businesses, as evidenced by the growing proportion of revenue stemming from enterprises with over $500K in annual receipts. This is a strategic move, as larger businesses offer a higher transaction volume than smaller merchants, ultimately translating to increased revenue potential for Square.

Square sees lots of headroom here, having captured only a tiny portion of potential mid-market customers.

Not A Hardware Company, But A Finance Company With Enabling Hardware

Although parallels can be drawn between Square's approach and Apple's design ethos, their core business models are fundamentally distinct.

Apple's core business revolves around hardware, with devices like iPhones and Macs accounting for a large share of its revenue. In contrast, Square's primary focus is financial services, generating income through payment processing fees and subscription-based add-ons.

Block’s 1Q’24 investor presentation makes it loud and clear:

We view hardware as an acquisition tool and not a profit center for our business.

Square's recent 10Q reveals that hardware isn't a profit center, with costs ($50.8M) exceeding revenue ($32.5M). However, this isn't a cause for alarm. Square strategically subsidizes hardware as a customer acquisition tool, offering it at a reduced price to incentivize adoption. The long-term bet is that the lifetime value derived from transaction fees and subscription services will far outweigh the initial hardware investment. This approach has been successful for Square over the past 15 years, indicating that the cost of acquiring a customer through subsidized hardware is less than the revenue they generate over their lifetime.

Square Hardware

As mentioned earlier, Square's commitment to delivering the best end-to-end experience for physical retailers has led it to focus on hardware innovation since its founding. Consequently, hardware design is one of Square’s core competencies.

Hardware-Enabled User Experience

We can see Square’s vision for a better payment experience enabled by hardware from the earliest days. Here’s a wonderful snapshot in time from way back in Dec 2009 with a young Jack Dorsey demoing the chip reader for TechCrunch:

MG Siegler: Hi this is MG Siegler with Tech Crunch. I'm here with Jack Dorsey, the creator of Twitter who's now working on a new project called Square. Hi Jack, do you want to tell us a little bit about Square?

Jack Dorsey: The basic idea behind Square is that everyone has this little plastic device in their pocket today which is a payment card – a credit card, a debit card, a prepaid card. They're using these things everywhere and they're using them to buy anything. It's really become this social interaction where no one thinks about the transaction anymore.

We we wanted to turn on the other side of that and allow people to very easily and quickly, within 10 seconds, be able to accept these plastic devices as payments and accept credit cards easily and efficiently. Really design the the product experience, really design the payment experience, which to my mind really hasn't been designed before. So that's that's what excites us.

To achieve this seamless payment experience, Square had to innovate simultaneously in hardware (the card reader) and software (the mobile app). This unique convergence of disciplines required a team comprising hardware and software engineers from the start.

Square has been a hardware-enabled finance company since Day 1.

Don’t Feed The Trolls

By the way, the comments on that 2009 video are hilariously representative of the kind of feedback the internet gives, ranging from armchair quarterback skeptics to impatient visionaries.

Skeptics:

“Dumbest idea ever heard. SLOW AS HELL”

“But who's going to trust it? That could be anybody's cellphone that's scanning (and potentially cloning) my credit cards”

That guy who is always trying to find a use case for augmented reality (even 14 years ago):

“This is a perfect AR app possibility.”

One comment even foreshadows Cash App:

i'm personally more excited for when customers can pay with their smartphones. but I can see the use for this. nice project.

The “nice project” bit also reminds me of Paul Graham’s How To Get Startup Ideas

Just as trying to think up startup ideas tends to produce bad ones, working on things that could be dismissed as "toys" often produces good ones. When something is described as a toy, that means it has everything an idea needs except being important. It's cool; users love it; it just doesn't matter. But if you're living in the future and you build something cool that users love, it may matter more than outsiders think.

At YC we're excited when we meet startups working on things that we could imagine know-it-alls on forums dismissing as toys. To us that's positive evidence an idea is good.

Specifically, the “nice project” comment felt like a “cool toy” remark.

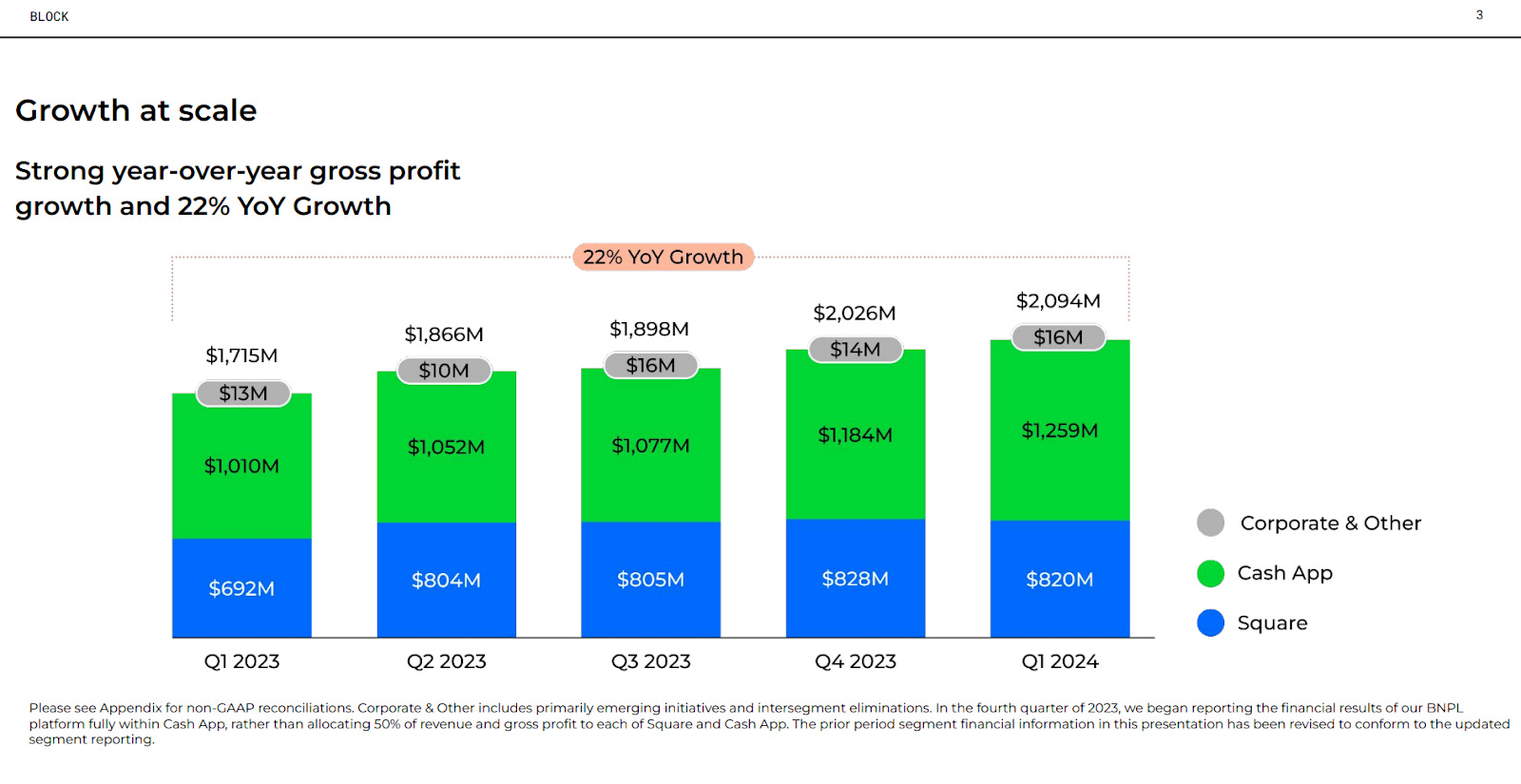

Regardless of what the internet know-it-alls thought, Square’s target audience was delighted with the product, and Square now generates $800M in quarterly revenue 😎.

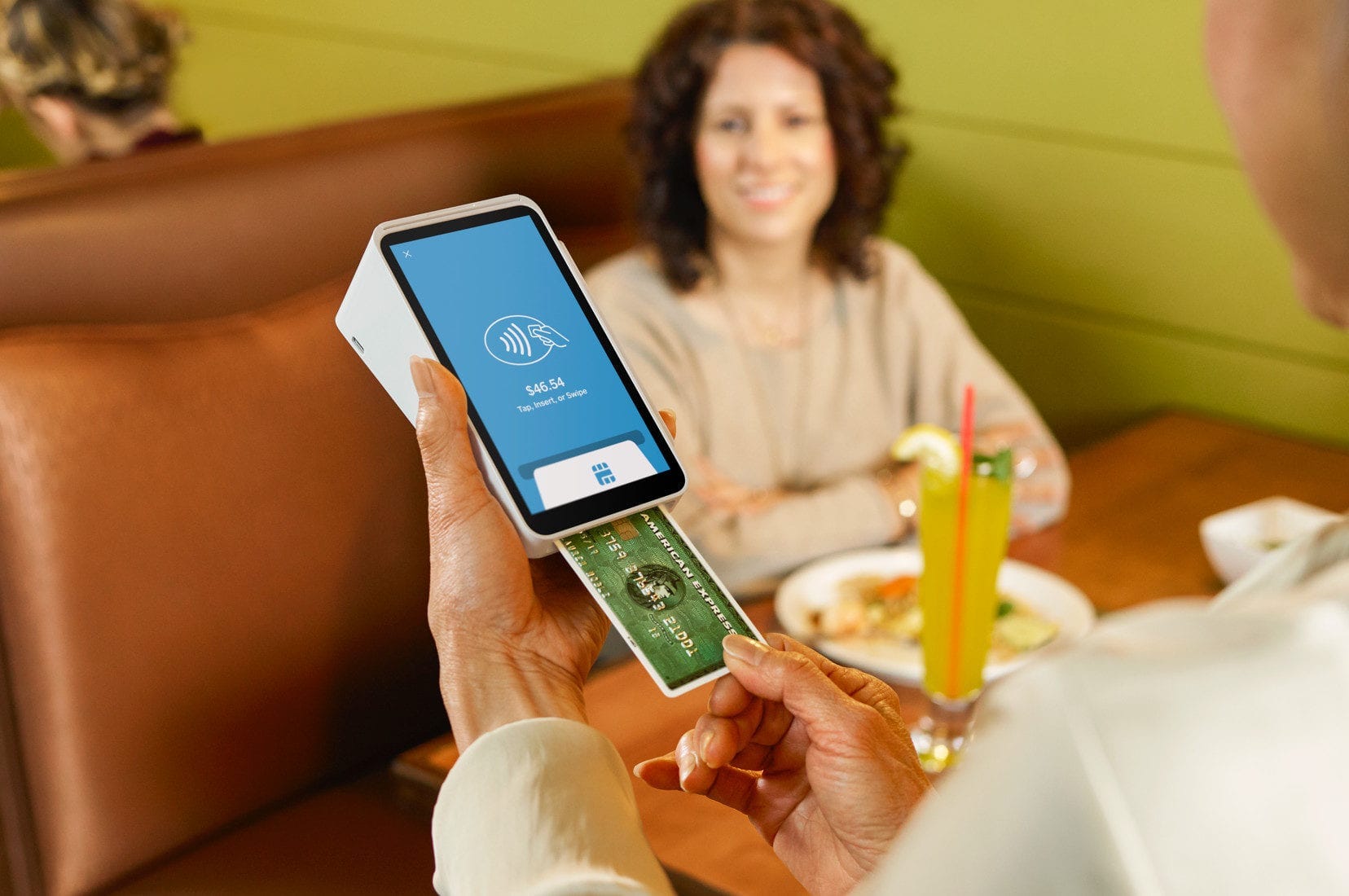

Mobile Reader

To truly appreciate Square's engineering acumen, let's take a closer look at their inaugural hardware product: the card reader. The product and engineering decisions that went into this device reveal a lot about Square’s product priorities and showcase its engineering chops.

Hint: The Square reader is incredibly elegant, yet robust enough to make the experience “just work” regardless of phone manufacturer or credit card provider.

Thanks to this 2010 Strangeloop conference talk from Square’s Head of Engineering and Android lead, we can get a good understanding of how their mobile card reader works.

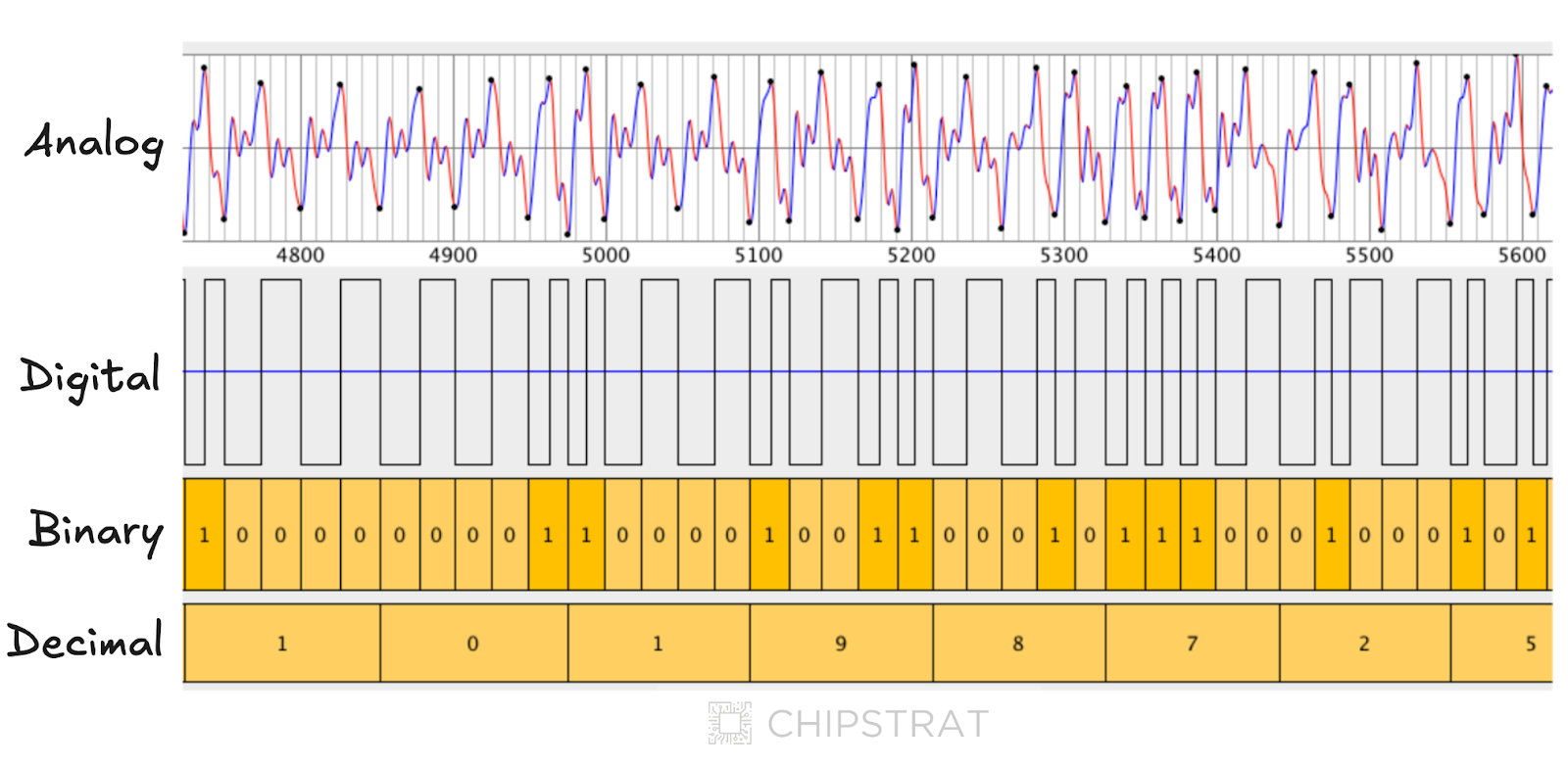

At its core, the solution is very simple: a magnetic card reader reads the swipe and transmits it as an analog signal over the phone’s headphone jack. Square’s mobile app then performs heavy signal processing to clean up the noisy analog signal and ultimately decode the card number.

Okay, so this is a Square. Tiny little thing, we give these away for free. Inside of here is a card reader, just a magnetic reader head, and a resistor. Other than that, that's it. It's a passive device. When you plug this into your phone, it acts completely as a microphone.

While this concept is straightforward, making a robust production implementation is complicated. Check out how complicated real life is! I’m sure any engineers out there can relate:

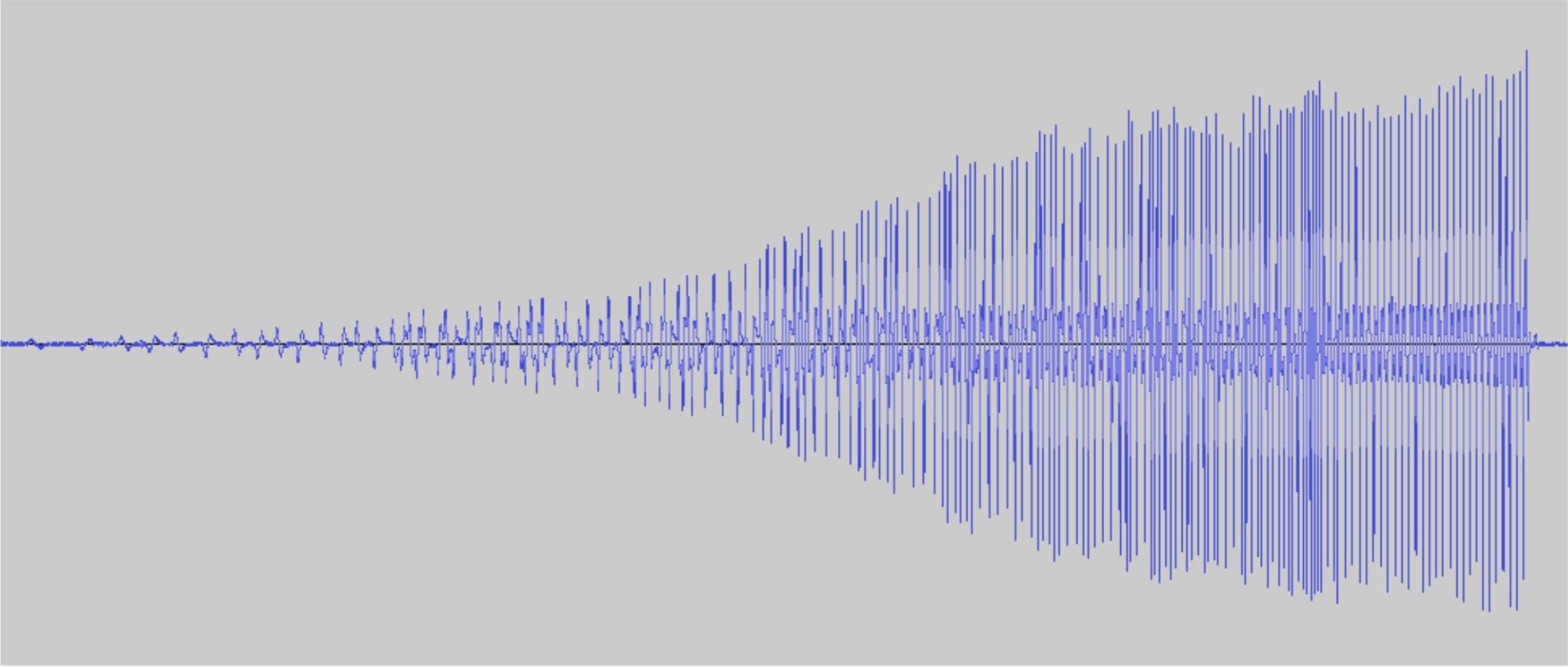

Let's take a look at a Motorola swipe recording. This a picture I grabbed from Audacity.

Basically, we swipe cards and capture a recording.

These are test cards. We have a card maker that makes fake data cards. We're actually not allowed to capture recordings from real credit cards for very obvious reasons.

But this is what it looks like. And you'll see it's very small at the beginning, and then the amplitude grows tremendously as it gets towards the end of the swipe. That's because when a human swipes a credit card, they always accelerate when they swipe across that reader.

Also, since it's a passive device, it's not actually powered in any way. The only way it gets power is from the magnetic stripe coming against that reader. So the faster you go, the higher the amplitude.

And also, it's really hard to see here, but these peaks are really close together as it goes faster and faster.

So if we zoom in to the beginning of the swipe, it doesn't look anything like that ideal waveform I showed you a few slides back, right?

This is a Droid. I've actually looked at enough of these. I can tell this is from Motorola device. All the Motorola phones do this, where you get the peak, but then it bounces back, and then you get another negative peak, and then it bounces up, and then goes up to here. It looks kind of shaky like this.

And the reason for that is the phones aren't designed for credit card processing. The phones are designed to capture audio from a headset. And what they do is they intentionally manipulate the audio to make it sound better. So that is the Motorola style of manipulating the audio to make it sound better.

So this is a real challenge for us, because on these devices it looks really nasty. And then towards the end of the Motorola swipe, it actually gets quite a bit easier – on the Motorola phones towards the end when you have nice big amplitudes, because these bounces are much less prevalent. But towards the beginning, it's a very difficult problem to solve.

More challenges with the swipe speed: Depending on who is operating the Square, they're going to swipe at different speeds. They might go really slow or really fast, or they might start slow and accelerate a whole bunch. So we have to account for as many of those variations as possible. Every human swipes differently.

If you're a beginner, you tend to rock the card. I'll tell you, there's basically nothing we can do about that. Once it moves off the read head, the signal gets corrupted. So with the square being so short, you really do have to practice a little bit and get a nice, smooth, even swipe.

The device sample rate varies between devices. We try to record audio at 48 kilohertz. That works on most Android phones. On the Samsung devices, though, if you record at 48 kilohertz, it bricks the phone. You have to actually take the battery out to get it to stop, because down the native code, the audio recording stuff saturates the CPU and it won't even react to the power button turning off.

What's worse is on those phones is if you ask it ahead of time, do you support 48 kilohertz? The phone says, yes, I do. So that was just a lot of trial and error.

We have special code in there, actually, to say if you're a Samsung phone, record at this frequency. That's actually one of the few spots in the entire app where we have anything device specific. We really try to write algorithms that adapt to whatever phone you're running on without us having to do checks. There's just too many Android devices for us to support. The Samsung phones were an unfortunate last resort. We had to do it to work around that bug.

Listening to this reminded me of an early lesson I learned when transitioning from engineering school to industry: Simple in theory, complicated in practice.

Square’s reader is a beautiful example of real-life hardware and software engineering working together. Clearly, Square prioritized creating elegant solutions that could generalize well across a broad range of inputs caused by the diverse set of supported phones, cards, and human operators.

If you have time, I recommend watching or listening to the entire talk for more interesting details regarding how the card reader works.

Terminal Teardown

Did Square's commitment to hardware excellence extend beyond its initial product?

I found this awesome Square Terminal Teardown blog to help answer this, including these videos:

In this case, Square didn’t build much new but instead leveraged the Qualcomm Snapdragon 615 platform, which is a mobile phone platform.

This makes a lot of sense. Square’s mobile terminal has many of the same needs as a phone: big display, portable, wireless connectivity, long battery life, and an operating system that makes building apps straightforward.

Innovate Only When Necessary

The decision to use Snapdragon illustrates Square's principle of creating hardware only when essential for differentiation.

The initial vision of “anyone can accept major credit cards on their phone” demanded hardware innovation with the Square reader. However, the mobile terminal can leverage many off-the-shelf components.

In addition to wiring up all of the components, we also see a Square custom chip on the security board, although I couldn’t find much information about what it does. That’s not surprising, given that it serves some sort of security-related purpose.

Based on the philosophy above, might this custom chip be necessary to differentiate the Square experience?

I’d be remiss not to call out that Square’s terminal includes several Arm-enabled chips.

Securing Hardware

Creating payment hardware requires developing expertise in preventing “tampering,” i.e., supply chain attacks that involve the insertion of unauthorized chips to siphon credit card data.

Square’s security module stores encryption information in volatile memory, powered by two small batteries that supply power even if the primary rechargeable battery is depleted. Removing the board will physically trip the tamper circuits and prevent the device from accepting payments. (Check out the videos to learn more.)

Realizing Square’s product vision necessitated developing domain-specific hardware engineering expertise.

NFC Reader Teardown

In this Square Chip and NFC reader teardown from All About Circuits, Square’s security proficiencies are on display again. I wanted to include some snippets from the article because it’s interesting and they include nice pictures.

When Square came out with their first hardware, they got a little bit of negative feedback due to its security (or lack thereof). This new device is more secure. Opening the device reveals a security housing covering the card slot and several of the ICs.

The security housing is made with a process called "Three-Dimensional Molded Interconnect Devices" or 3D-MIDs. This process uses an injection-molded part that has conductive traces applied to it using a laser-directed structuring process. If any of the conductors are broken or the housing is separated from the PCB, the encryption key is erased.

The security housing makes contact with the PCB using four elastomer connectors. These touch the plated contact on the security housing and the exposed copper contacts on the PCB.

This chip reader uses two primary coin cell batteries to store the encryption information in volatile memory. These batteries supply power even if the primary rechargeable lithium polymer battery is depleted. In addition, the connections associated with this circuit are interconnected through blind vias, making it difficult to bypass or jumper around the tamper circuit.

Even this seemingly innocuous card reader contains three Arm cores:

It's also worth noting that the Bluetooth radio IC used in this device also has a programmable Cortex-M3 core and a Cortex-M0+ in it’s RF core. That is a total of three ARM cores in this one device.

Product and Engineering Competencies

Square demonstrated an ability to balance pragmatism and innovation in hardware development. They focused on delivering exceptional user experiences, utilizing off-the-shelf hardware whenever feasible, and only innovating when necessary to set their products apart.

As the secure hardware exploration demonstrated, Square has developed significant knowledge of payment processing hardware and software. This gives Square a nice headstart and an advantage over any new competition.

Payments are complicated, sensitive, and highly regulated, and this domain knowledge can’t be acquired overnight.

Most importantly – Square has developed strong consumer-grade product development capabilities. Specifically, Square builds consumer-grade products with beautiful industrial design and a clean user interface that requires little to no training.

Square Applies The Apple Ethos To Payments

At first blush, a heavy emphasis on consumer-grade product design is an interesting decision because Square’s customers are businesses. And if there’s one thing we know about business-to-business (B2B) products, it’s that the people writing the check (often not the actual end-user) will accept user experiences are notoriously subpar.

But Square threw out the status quo and elevated product design to the highest standard. It also helps that the micro and small business decision-maker paying for the product is often also the person using it.

The focus on impeccable product design reflects the founders' high design standards. Recall that Jim McKelvey is an engineer and an artist. From STLMag,

On designing a Square card reader that was so small, it only worked 80 percent of the time—and why he didn’t go bigger:

No good engineer—and I consider myself a good engineer—would do what I did. I built something that didn’t work as well as something else that I built. Oh, and by the way, we manufactured both of those. It wasn’t like these were prototypes. I actually ran 40,000 of the big ones and 40,000 of the little ones. The little one didn’t work as well as the big one, but the little one had this magical spell, and I thought the magic spell was probably important. Even though there’s no management course on magic spells, there’s no way to explain cool, there’s no way to explain beauty. The risk was trusting my instinct—I had data against the little unit. The little unit read 80 percent of the time, and the big unit read 100 percent of the time. But there was also this feeling, and maybe my years as an artist gave me a respect for that feeling. It was something that tugged at me.

Strong echoes of Steve Jobs right there.

This Ethos Is Strategically Sound

Square’s guiding principle of building consumer-quality hardware is also strategically sound. Consider a POS transaction between a buyer and seller. The buyer may not be familiar with Square’s system and must intuitively understand how to proceed. On the other hand, the seller might have limited training yet needs to manage the transaction efficiently. A frictionless exchange is essential for both buyer and seller.

Nothing kills retention like a painful, slow, or awkward checkout process.

Envisioning The Future

Finally, Square has shown an ability to deeply understand the customer journey and create a better solution than the status quo.

Customers appreciate this. Note the number of Square customers who pay for multiple products—they not only trust Square with their payments, but also want as much help from Square as they can possibly get.

Random GenAI-Related Thought

Square’s terminal uses a Qualcomm chip with a Hexagon DSP. This is the same Hexagon DSP Qualcomm used as the foundation of their NPU.

It’s interesting to brainstorm how these POS might benefit from upgrading to a Snapdragon with an NPU. Could running a fine-tuned model on the POS improve the transaction in any way? Maybe with fraud detection or upselling a customer?

Cash App

The Cash App doesn’t have a hardware angle, but we’ll quickly cover this business as it’s an important context for Block’s Bitcoin endeavors.

If you’re unfamiliar with Cash App, have you heard of Venmo? Cash app is Venmo’s twin. Both are apps that allow people to send and receive money electronically.

Like Square, Cash App has expanded beyond its initial use case to solve many related problems.

Cash App provides an ecosystem of financial products and services to help consumers manage their money. Cash App’s goal is to redefine the world’s relationship with money by making it more relatable, instantly available, and universally accessible. While Cash App started with the single ability to send and receive money, it now provides an ecosystem of financial services focused on helping consumers make their money go further by enabling customers to store, send, receive, spend, invest, borrow or save their money with Cash App.

Cash is a profitable and growing business:

Did you notice the focus on “ecosystems”? Both Square and Cash App connect buyers and sellers and offer a variety of related services.

Square elevates the physical payment experience, and Cash App does the same for digital payments.

TIDAL

After Square added Cash App, it reorganized into a parent company (Block) with subsidiaries (Square, Cash App). Block also has other companies in its portfolio including TIDAL, a high-fidelity music streaming service.

Jay-Z bought TIDAL for $56M in 2015, sold 33% ownership to Sprint for $200M in 2017, and then sold a majority stake to Block for a $297M mix of cash and stock.

On April 30, 2021, the Company [Block] acquired an 86.8% ownership interest in TIDAL, a global music and entertainment platform that brings fans and artists together through unique music, content, and experiences. The acquisition extends our purpose of economic empowerment to musicians.

Honestly, Block’s acquisition of this business is hard to rationalize.

One explanation is that Block’s acquisition of TIDAL occurred during the height of the NFT craze. Block has a digital payments transaction platform (Cash App) and Bitcoin aspirations, so it’s conceivable that Block wanted to move into the NFT space and saw TIDAL as a means to acquire relationships with artists.

A less flattering contribution might be the allure of celebrity; Jay-Z is now on Block’s board of directors.

Square’s official explanation painted the acquisition of Tidal as a strategic investment to (somehow) integrate Tidal’s platform with Square's commerce and payment capabilities.

The acquisition extends Square’s purpose of economic empowerment to a new vertical: musicians. Artists are entrepreneurs with a dream and deserve access to systems, tools, and financial freedom to reach those dreams at every stage in their career. Square has helped millions of businesses start, run, and grow by providing them with tools needed for success. With Cash App, Square has made financial services more relatable and accessible to millions of customers, many of whom have been historically overlooked and underserved. Square sees an opportunity to leverage those learnings to help musicians find new ways to support their work and make better decisions through TIDAL.

“It comes down to one simple idea: finding new ways for artists to support their work,” said Jack Dorsey, cofounder and CEO of Square. “New ideas are found at intersections, and we believe there’s a compelling one between music and the economy. I knew TIDAL was something special as soon as I experienced it, and it will continue to be the best home for music, musicians, and culture.”

The “finding new ways for artists to support their work” quote reinforces my thinking about an NFT play.

The funny thing is I’m currently wearing a T-shirt I bought at a merch table during a concert. I paid for this shirt with a credit card using a Square mobile reader, so Square (Block) is already helping musicians make money in the physical world.

I'm not sure where Block could fit into the existing online music value chain as far as digital payments go.

Of course, I also paid a ticketing company for the privilege of watching that band live, and ticketing is a really hard market to enter, so I doubt Block will try to capture a piece of that transaction.

If Block was trying to find new value chains for artists, my only explanation is NFTs. If anyone else has a better idea, I’m all ears.

Ecosystem of Ecosystems

Finally, we see Block trying to apply the “ecosystem” playbook across its subsidiaries, which they call an “ecosystem of ecosystems.”

At Block, Inc. (together with its subsidiaries, "Block" or "we"), we are building an ecosystem of ecosystems, each focused on distinct customer audiences. We define an ecosystem as a set of tools and services that work together cohesively, often positively reinforcing one another. This helps create resilient relationships with customers as they use our tools and services to satisfy multiple needs. Our ecosystems are united by our shared purpose of economic empowerment, with each ecosystem serving different people — sellers, consumers, artists, fans, and developers. As we scale, we are focused on investing in developing connections between our ecosystems and by creating more connections to increase the resilience of our overall company.

I buy the “ecosystem” approach for both Square and Cash App. Strategically, these ecosystems are very complementary. There’s likely shared infrastructure and domain knowledge underlying physical and digital payment ecosystems, so the line about “developing connections between our ecosystems” rings true.

But is TIDAL an ecosystem?

Sure, it’s a network between listeners and musicians. And yes, I can imagine building a suite of tools and services around that network… because Spotify already does that with tools for artists, podcasters, advertisers, and listeners.

Should TIDAL follow suit? Is there room for another Spotify?

Not all playbooks are one-size-fits-all.

I hope you enjoyed this tour of Block’s hardware competencies and core businesses. Next week, we’ll use what we learned in this post to unravel Block’s Bitcoin ambitions, with a special focus on their 3nm Bitcoin mining ASIC and self-custody Bitcoin hardware wallet.