Rethinking Amazon + Not All SaaS Is Dead

AWS Shows a Survival Path for Enterprise Software

I’m updating my priors on Amazon.

On Monday, Microsoft and OpenAI amended their partnership. OpenAI is no longer exclusive to Azure; the license is now non-exclusive; OpenAI can serve all its products on any cloud. Like AWS.

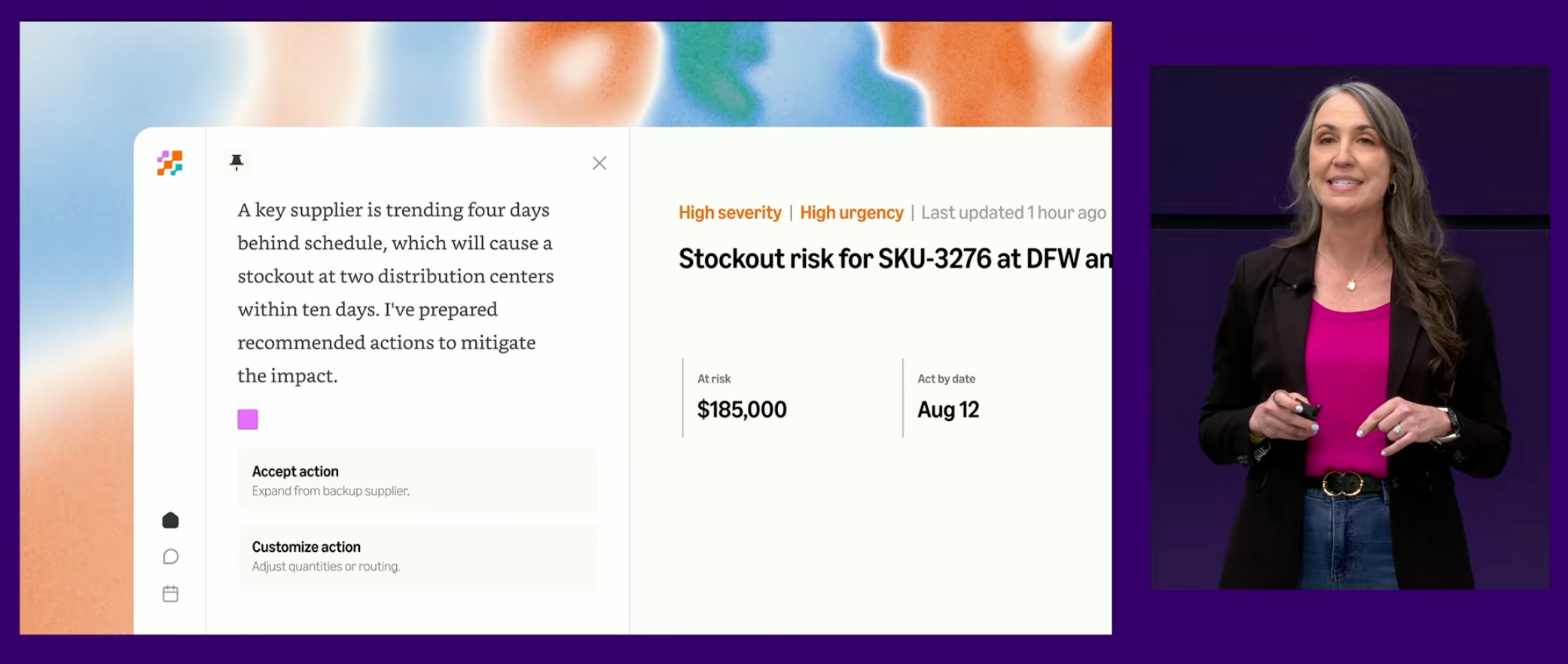

On Tuesday, AWS launched Bedrock Managed Agents (powered by OpenAI) along with the new Connect family of agentic enterprise apps.

The same day, Ben Thompson published a joint Stratechery interview with Sam Altman and Matt Garman explaining the partnership.

By the way, AWS CEO Matt Garman is on X now! Less than 3K followers at time of writing. That will surely change:

Lastly, on Wednesday AWS posted very strong Q1 2026 results.

What to make of it all?

I’ve long been a bit bearish on Amazon. AWS is a phenomenal business, but at the corporate level it pulls Amazon’s margin up because retail is a tough low-margin business. Google is the inverse: GCP pulls Alphabet’s margin down because Search and ads print money. I’d rather be Google.

And my bearishness persisted. I hoped Amazon would see the AI shift as an opportunity to pour resources into AWS and expand its dominance and profit dollars, but instead, Azure and GCP ran ahead in GPU capacity. Plus Azure had an exclusive relationship with OpenAI, and Google’s own Gemini models seemed to keep up.

Man. If alpha was in the model, and GPUs powered frontier models, AWS didn’t have enough of the asset that mattered. Although Anthropic was showing some early promise…

But the agentic era is quickly changing things. No truer words, right?

The agentic platform, as I’ll explain, is sticky and value-accretive. AWS has an opportunity here. Moreover, Amazon’s Graviton and Trainium are well-positioned to serve it cost-effectively. And most importantly, Amazon’s own e-commerce operations are the best possible first customer for agentic platform primitives. But a platform needs an ecosystem, and SaaS is dead right? Nope. AWS shows a survival playbook for other operationally-grounded SaaS companies. And Connect family revenue is gravy on top, too.

Right now, AWS’ future looks bright; if they deliver on the vision, we’re in a period with dual mispricing opportunities for investors: