Micron's Blowout and the Case for a Memory Supercycle

Micron's GM hit 84.9%, it booked $10B of take-or-pay through 2030, and supply shortage stretched further out. Peak? When does supply increase? SK Hynix and Samsung too.

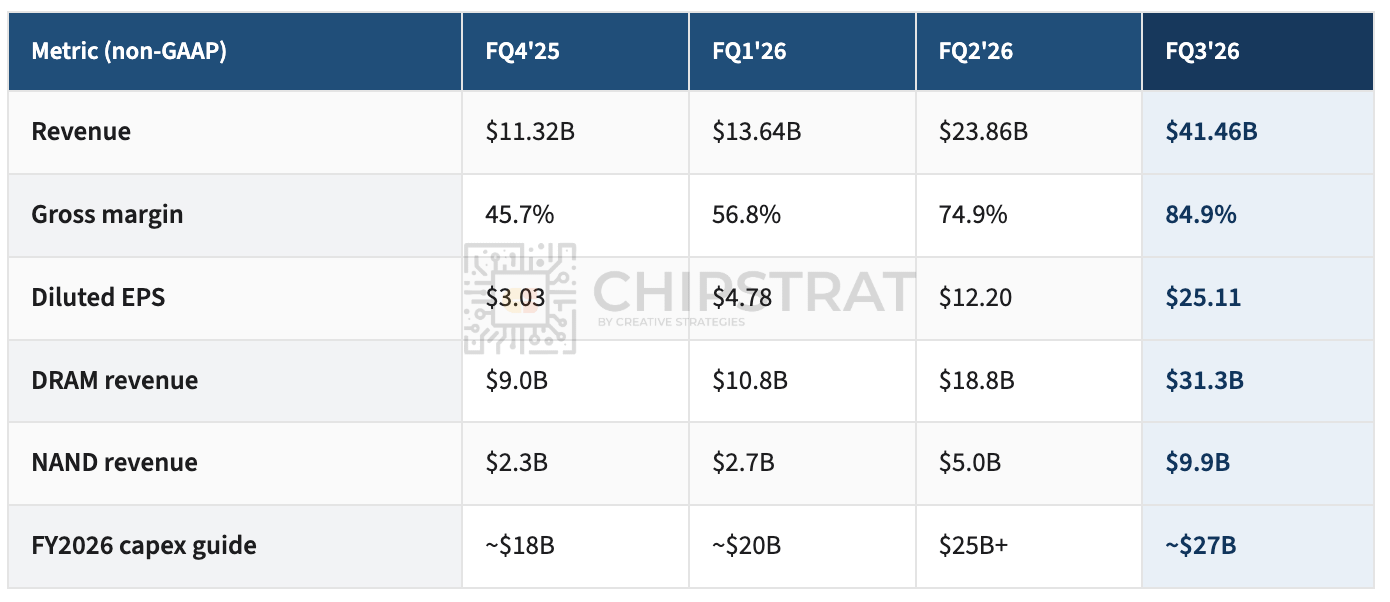

As you probably heard, Micron crushed earnings this week. It got me thinking. Man, Micron has come a long way in the past year.

Just look at the past four quarters:

Revenue went from $11.3 billion to $41.5 billion. Gross margin went from 45.7% to 84.9% (!!!)

Each quarter beat the guidance Micron gave the quarter before, and the magnitude of the beat grew each time.

And here’s a mind-bender. Micron’s fiscal Q3 revenue of $41.5 billion was larger than its revenue in any previous full year in company history. Bigger than the $37.4 billion it booked in all of FY2025. Bigger than the prior record of $30.8 billion in FY2022.

Of course, what does that margin chart scream for folks who’ve been around the block? Peak. Memory is the most cyclical business in semiconductors. It’s like a sine wave:

That nice little rolling wave there is the semiconductor cycle.

I love how Doug O’Laughlin visualized the cycle here with various markets moving around on a merry-go-round:

Think of memory’s revenue wave as the weighted average of all the memory-consuming semis markets. Each one sits somewhere on the merry-go-round and carries weight equal to how much memory it buys, so the cycle you see in Micron’s revenues is really just the combined center of mass.

Which raises the question… which quadrant is that center of mass in now, and what would tip it into the next one (top right)?

Well, the merry-go-round still exists, it’s just that the mass of datacenter AI is sooo big that all the other kids on the merry-go-round don’t meaningfully contribute to the center of gravity as much anymore. AI is the dad who jumped on the merry-go-round with a couple of three-year-olds. Dad’s weight wins.

And yeah, I cropped that earlier Micron revenue chart for dramatic effect. Here’s what it looks like now:

YO! The amplitude of that sine wave is much bigger!

So let’s dig into that demand more and figure out if and when more supply is coming online. Can supply counterbalance, or will this memory supercycle persist?

Behind the paywall:

Demand has two drivers… and don’t forget NAND: HBM is stacked DRAM, so it pulls many wafers off the DRAM market, right as server CPUs pull from the same pool. And AI is eating NAND too.

The shortage goes out through 2027: CapEx up by half while the shortage horizon slid out a full year, and the construction-clock, node-shrink, and cleanroom limits behind it.

What the contracts change: sixteen take-or-pay deals lock ~20% of DRAM and a third of NAND to 2030

SK Hynix and Samsung say it on their own calls: the supply-demand gap widening into 2027, demand for the next three years above capacity, DRAM ASPs up ~60% in a quarter, HBM “sold out”.

What still cuts the other way: ~80% of DRAM still reprices with the market, and Micron’s own guide already flags a “moderation in the rate of price increases”.

The scorecard: the handful of variables that decide persist versus revert, each with a read and a date.